The Markets week in review and Economic Climate

for the

Week Ending June 24th 2022

The content of this Newsletter is to provide you with Economic insights to assist you in making better decisions with your investments. Unlike many other financial periodicals we will not mention specific companies, unless it is relevant to an overall economic issue. We welcome your questions on economic concerns and will address in our newsletter. just email us at info@optfinancialstrategies.com #FinancialAdvisor,#investmentmanagement #wealthmanagement #financialplanning #retirementplanning #401kplans

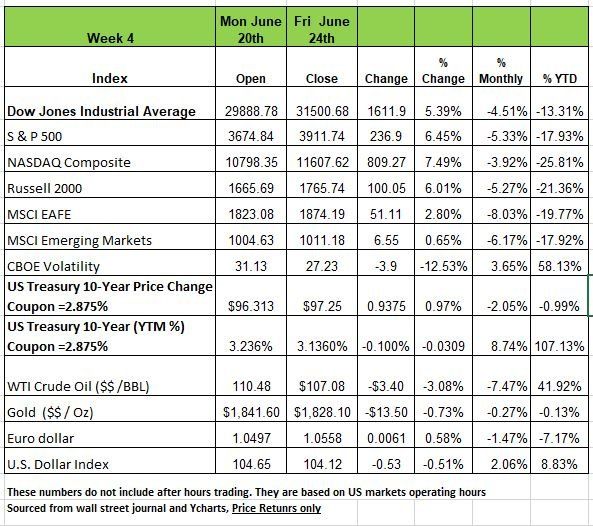

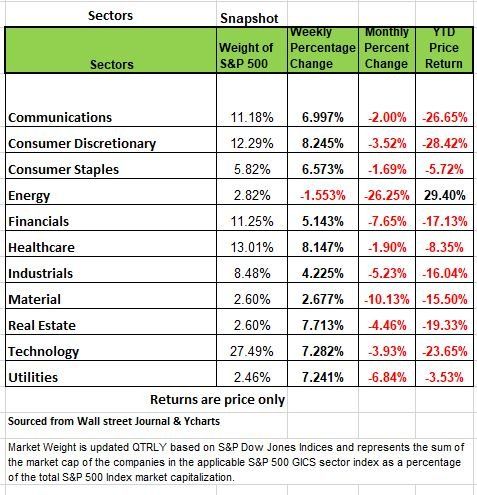

U.S. equities bounced up after a sharp drop in commodity prices and interest rates last week. The Nasdaq Composite Index jumped 7.5%, while the S&P500 and Russell 2000 added 6%+ point and the DOW pulled up the rear with a positive 5.39% increase. 10 of 11 S&P500 sectors were higher, with energy the lone loser. Crude oil fell 1.25%, while copper prices plummeted 9% before recovering some losses as traders eyed a precarious global economy.

Treasury yields corrected after Fed Chair Powell told Congressional committees that the central bank’s inflation fight is “unconditional” but acknowledged that a recession is possible. Which seem to conflict with Janet Yellen take in stating again that there were no signs of a recession

The housing market continues to struggle with high mortgage rates, as existing home sales slumped 3.4% in May while the median sales price surged to a record $407.6K. New home sales rose unexpectedly but the rebound is likely to be temporary as affordability is squeezed.

Consumer sentiment was revised slightly lower to yet another historic low, but inflation expectations softened marginally.

Yields fell across the curve during last week’s holiday shortened week. Poor economic data and hawkish comments from Federal Reserve officials perpetuated recession fears leading many to believe the current rate hiking cycle will be shorter-lived than previously thought. On Thursday, PMI manufacturing came in at 52.4 vs 56.0 expected, and new orders tumbled from 54.4 to 47.7 – the first-time new orders fell below 50 since July 2020.

Internationally, Germany’s business sentiment worsened in June as the natural gas supply for Europe’s largest economy looks increasingly uncertain. Producer prices jumped 33.6% YoY in May and 16.5% excluding energy. In the UK, CPI hit 9.1% YoY in May, curbing retail sales as consumers pulled back on soaring grocery costs. Finally, Japan’s consumer inflation exceeded the central bank’s target for a second straight month but still lags well behind other developed economies at 2.1% YoY.

Oil Price Reversions – The Inevitable Outcome Of Recessions

A price reversion states that price volatility is generally only temporary. When an asset or a commodity has extreme price swings, eventually it will return to its long-term average. This concept can apply to virtually any financial metric or commodity. Hence Oil prices along with energy stocks may be starting its price reversion. The reason is that oil price reversions are the inevitable outcome of an economic recession. This is due to the price spikes that created the demand destruction in the economy.

Higher oil prices benefit oil companies by making the extraction process more profitable. However, there is also a negative impact on the economy.

“High oil prices add to the costs of doing business which pass, ultimately, on to customers and businesses. Whether it is higher cab fares, more expensive airline tickets, the cost of apples shipped from California, or new furniture shipped from China, high oil prices can result in higher prices for seemingly unrelated products and services.” – Investopedia

Consumers who fill up their gas tanks each week immediately notice high oil prices. The last time I filled up my car, I noticed drivers taking pictures of the price to fill up their tank. Most are north of $100. Something consumers have never experienced. While the national average is now below $5/gallon many cities like Chicago are experiencing higher prices due to the tax the city state and county place on each gallon of gas.

While core inflation reports strip out food and energy, those items drive short-term consumption patterns.

Given that consumption comprises roughly 70% of the GDP calculation, the impact of higher oil prices is almost immediate.

Spikes in oil prices have a high correlation with economic recessions, financial events, and oil price reversions.

Oil prices are crucial to the overall economic equation. As prices increases, it translates into higher inflationary costs to consumers. Unsurprisingly, there is a high correlation between the rise and fall of energy prices and the consumer price index.

Oil prices impact virtually every aspect of our lives, from our food to the products and services we buy. Therefore, the demand side of the equation is a tell-tale sign of economic strength or weakness. Oil prices track our combined rates, inflation, and GDP index.

The oil industry is very manufacturing and production intensive, rising oil prices increase manufacturing, CapEx, and economic growth. This also works in reverse.

“It should not be surprising that sharp spikes in oil prices have been coincident with downturns in economic activity, a drop in inflation, and a subsequent decline in interest rates.“

The most recent surge in oil prices resulted from the massive flood of fiscal policy and a supply shortage. Yes, the Russia /Ukraine conflict contributed to the situation but what had more of an impact was an aggressive political and Wall Street “green energy” campaign which restricted drilling and refinery production. Those policies reduced capital formation for drilling projects and removed oil exploration incentives.

While the pandemic-driven shutdown of the economy created a supply shortage, the flood of liquidity created a demand surge. That “pull-forward” of consumption led to surging inflationary pressures and rising oil prices.

Naturally, slower economic growth and deflationary pressures will contribute to an oil price reversion as consumers opt to drive less. Personally, I started to bike to work, the weather is nice and I need the exercise.

While the recent rally in energy stocks has been quite strong, the Fed’s aggressive tightening monetary policy with the sole goal of combating inflation will slow economic growth, which reduces demand for commodity-based products.

Unfortunately, if history repeats, it won’t be just oil prices and energy stocks that get brought down in the process. Source https://realinvestmentadvice.com/oil-price-reversions-the-inevitable-outcome-of-recessions/

What to think about before retiring?

There are a few terms in behavioral finance that you should be aware of before you actually pull the trigger when retiring. Each of us has some “Financial Achilles Heel” when it comes to money. One of the most common is mental accounting. Mental Accounting is a concept in behavioral economics that mainly refers to a cognitive bias in the way people treat money in different categories (buckets). Money is money it should all be treated the same. When it comes to retirement this becomes extremely important. This bias can lead to mistakes that can eventually cost you a lot of money. Being over conservative can lead to running out of money.

Having a written plan and budget in retirements can help if you can discipline yourself to sticking to it. Having a portfolio that generates income so you do not have to liquidate assets in order to get money is also important. If you have been one of the many that has invested in Index Funds and ETF’s over the last 20 years you might want to evaluate the dividend and interest income that your portfolio throws off. Many advisors typically have a dividend reinvestment function turned on so any income generated automatically gets reinvested. In retirement this is not a good philosophy. Because the investors need to liquidate positions in order to get cash. a retirement portfolio should be designed to generate cash so that regardless of the fluctuation is the value of your portfolio it is still generating income. Of course, this is based on a company not suspending its dividend payments. Look closely at your holdings, make sure you are maximizing income on your investments.

Bidding Wars Overheated the Home-Buyer Market, Now They’re Coming for Renters

If you thought that buying a home was challenging during the pandemic try renting a place to live. America has a housing shortage. New building permits have dropped significantly meaning home builders have reduced the number of projects they are doing. Cost of material and labor is just one reason. Interest rate hikes have also cut the profit margin down and the demand for homes. This has led consumers to rent. But the demand on rentals has increased leading renters to now offer more on properties that they want. Rent is 30% of the weight in the calculation of CPI. During the pandemic when many people fled larger metropolitan areas leaving many landlords with a high number of vacancies. In addition, many other renters took advantage of the eviction moratorium and did not pay rent. Its now payback time and landlords are finding themselves in a market that is short on supply and higher in demand. Source https://www.wsj.com/articles/bidding-wars-overheated-the-home-buyer-market-now-theyre-coming-for-renters-11656322200?mod=hp_lead_pos12

Changes for credit reports made jointly by Equifax, Experian, and TransUnion

The three nationwide credit reporting agencies - Equifax, Experian and TransUnion - have agreed to three important changes to reporting medical collection accounts

Paid medical collection debt will no longer be included on consumer credit reports, as of July 1, 2022.

The time period before unpaid medical collection debt will appear on a consumer’s report will be increased from six months to one year, also effective July 1, 2022. This change gives consumers more time to work with insurance and/or healthcare providers to address medical collection debt before it appears on credit reports.

Medical debt collection accounts under at least $500 will no longer be included on consumer credit reports. This goes into effect the first half of 2023. These significant changes to medical collection debt reporting support consumers faced with unexpected medical bills and can payoff the debt over a longer period of time without impacting their credit scores.

A Technical Perspective

Technical analysis is a trading discipline employed to evaluate investments and identify trading opportunities by analyzing statistical trends gathered from trading activity, such as price movement and volume

After a federal holiday last Monday, the S&P 500 rallied for the week, this included two outlier days of +2.45% and +3.06%. As a reminder, an outlier day is any single trading day beyond +/-1.50%. As we wrote last week, “Through the first 6 months of 2022, you would expect see about 6 outlier days beyond +/-1.50% [based on bell curve math during a normal, efficient market environment].”

The number of outliers in 2022 is now up to 43 outlier days. Again, in a normal market environment, you would expect to have 6 days. The S&P 500 has had seven times as what was expected. This is reflective of a highly volatile bear market environment.

Bear markets, like we are seeing today, will feature large rallies. Last week’s outliers were two very large “up” days, but that doesn’t mean we are seeing a shift in market environments. In fact, volatility is going up, not down. Our Volatility Index (VI) is now at a 2-year high. High volatility is the primary characteristic of a bear market. In order to for the bear market to change to a bullish or transitional Market State, two things would need to occur.

To change from a bear to a bull/transitional market environment:

Volatility needs to decline by at least 20-30%. Right now, volatility is at VI 146. Generally speaking, a volatility less than VI 75 is considered low and stable.

So we need to see is a series of higher highs and higher lows. Bull markets are characterized by a steady and slow, upward climb where the markets put in a high, and then pullback and put in a low, followed by a rally to a higher high and pullback to a higher low.

Right now, we have only seen lower highs and lower lows. It will take time for this process to play out.

Across the board, every global equity ETF in our universe (which is about 150 ETFs) is in a Bearish Market States. Keep in mind that there are several ETFs “alternatives to global equities” category that are in Bullish Market States, most of which are inverse ETFs. (Betting against the market)

Energy

The energy sector has been the best performing S&P 500 sector in 2022. Recently, the sector has experienced a large pullback. Right now, it appears to be sitting on support. The ideal scenario is for the group of energy stocks to bounce upward off this support level. But keep in mind as we mentioned above, we do expect a price reversion which would impact energy company prices.

Source Brandon Bischoff

The Week Ahead

The decline in commodities and yields last week generated some optimism on inflation expectations and the pace of future rate hikes. But as Fed Chair Powell said in his testimony, the central bank needs “compelling evidence” that prices are falling and won’t ease off hiking rates until inflation is under control. That puts this Thursday’s U.S. PCE Price Index release in the spotlight, and consensus estimates point to a second straight monthly drop in the core reading.

A busy U.S. calendar also includes durable goods, consumer confidence, trade balance and inventories, and personal income and spending figures. The week closes with the ISM Manufacturing PMI report. The oil and gas markets may react to the G7 meetings that began yesterday, where global leaders will discuss measures to stabilize energy prices.

The ECB will host a forum on central banking in Portugal mid-week, another opportunity to hear the leaders of the ECB, FOMC, BOE and others opine on monetary policy. Eurozone inflation updates also appear with German CPI on Wednesday and EU flash CPI on Friday.

In Asia, the yen’s collapse has traders thinking the BOJ will relent and eventually raise the ceiling on bond yields, with inflation statistics and business surveys due on Friday.

This article is provided by Gene Witt of FourStar Wealth Advisors, LLC (“FourStar” or the “Firm”) for general informational purposes only. This information is not considered to be an offer to buy or sell any securities or investments. Investing involves the risk of loss and investors should be prepared to bear potential losses. Investments should only be made after thorough review with your investment advisor, considering all factors including personal goals, needs and risk tolerance. FourStar is a SEC registered investment adviser that maintains a principal place of business in the State of Illinois. The Firm may only transact business in those states in which it is notice filed or qualifies for a corresponding exemption from such requirements. For information about FourStar’s registration status and business operations, please consult the Firm’s Form ADV disclosure documents, the most recent versions of which are available on the SEC’s Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov/

The Optimized Investor