Economic and Market Climate

for the Week Ending August 5th 2022

The content of this Newsletter is to provide you with Economic insights to assist you in making better decisions with your investments. Unlike many other financial periodicals we will not mention specific companies, unless it is relevant to an overall economic issue. We welcome your questions on economic concerns and will address in our newsletter. just email us at info@optfinancialstrategies.com #FinancialAdvisor,#investmentmanagement #wealthmanagement #financialplanning #retirementplanning #401kplans

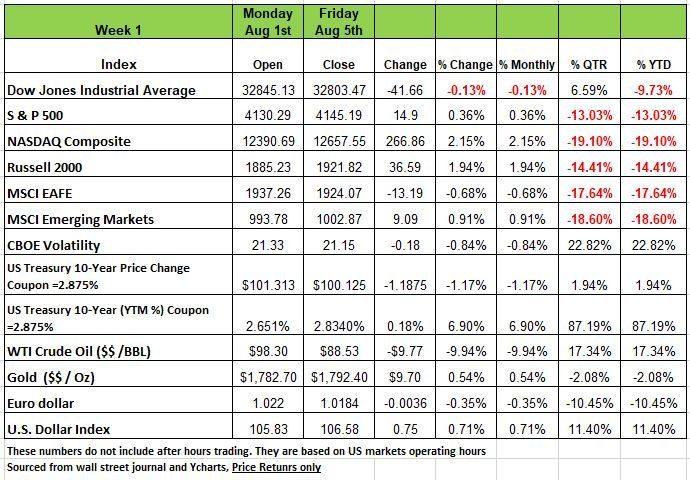

Three of the Four major indices finished in positive territory last week with the DOW having the only negative return on the week with a -.13% decline. U.S. equities wavered during the week but finished positive after a surprisingly strong jobs report, +528K increase in June, (the number is more than double expected). This led the markets to be concerned that the FOMC is likely to stay on an aggressive rate-hiking path but Wednesdays CPI number for July YOY will have a lot of weight on how the Fed reacts. The S&P500 Index ended marginally higher, while the Nasdaq Composite and Russell 2000 gained 2% & 1.94% respectively.

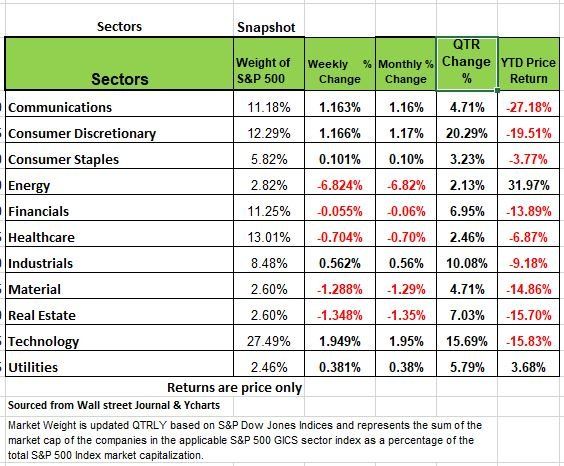

Sector performance was mixed with 7 of the 11 sectors finishing up, with energy stocks having the largest movement -6.8% selling off after crude oil plunged more than 10%. OPEC agreed to only a modest production increase and U.S. stockpiles unexpectedly surged. Technology was the big winner last week with a price return of 1.95% follow by communications and consumer discretionary both with +1.16% the rest of the sectors came in +/- a few basis points.

U.S. manufacturing PMI cooled in June as new orders shrank and inventories rose, while services activity expanded. Both reports’ employment components contracted. The U.S. trade deficit declined but is still 33% higher than a year ago as domestic supply has lagged strong demand.

On the International front, the Bank of England increased rates by 50bps while saying that Britain should expect a lengthy recession. The RBA instituted an identical rate hike, further pressuring Australia’s highly leveraged housing market. In Europe, Germany’s retail sales dove 8.8% YoY in June and factory orders shed 0.4% MoM as inflation and the war in Ukraine weighed. Canada’s economic activity stalled for the first time this year as employment levels fell for a second consecutive month in July and Ivey PMI contracted. Finally, China’s services PMI grew at the quickest pace in 15 months, but the country’s manufacturers struggled on weak foreign demand.

U.S. Treasury yields rose significantly over the course of the week, especially short-term yields, as investors weighed the pace at which the Federal Reserve would increase interest rates at coming meetings. Yields started the week with a drop in rates on Monday, before rising significantly on Tuesday as regional Fed policy makers Mary Daly and Charles Evans said that U.S. interest rates need to keep rising until inflation comes back down. Long-term yields then dropped moderately again on Wednesday as the ISM manufacturing index rose to a 3-month high of 56.7, compared to estimates of 55.3. Yields remained flat on Thursday as the Bank of England increased their target interest rate to by 50 basis points to 1.75 and U.S. Jobless claims met expectations of 260k.

On Friday, yields rose significantly again across all durations with July’s job report. This led investors to speculate that the Fed may increase the Federal Funds Target Rate more rapidly. The market implied probability of a 75- basis-point increase at the September 21st meeting rose from 32% at the beginning of the week to 76% by the end of the week. The yield curve continued to invert as the 2-year yield ended the week 40 basis points higher than the 10-year yield. Historically this has always predicted a recession. Oil prices dropped 10% over the course of the week as recession fears have led investors to speculate there will be reduced demand for oil.

Major economic reports for the upcoming week include: Wednesday: MBA Mortgage Applications July CPI MoM & YoY; Thursday: Initial Jobless Claims, July PPI Final Demand MoM & YoY U. of Mich. Sentiment

No Recession? Then why are Yield Spreads Are Collapsing

We are not really sure why a professional with such a poor track record of forecasting economic downturns is consistently asked about the state of the economy. Treasury Secretary Janet Yellen, recently declared that there was “No Recession” noting that consumer spending, industrial output, credit quality, and other indicators don’t suggest economic risk. What information is she looking at!

“You don’t see any of the signs. A recession is a broad-based contraction affecting many sectors of the economy. We just don’t have that. We’ve cut the deficit by a record one and a half trillion dollars this year. We’ve seen gas prices come down by about 50 cents in recent weeks, and there should be more in the pipeline. And hopefully, we will pass a bill that will lower prescription drug costs and maintain current levels of health care costs.” We expect that Ms. Yellen will soon say that we did not see this coming like other economic downturns that she was incorrect about. But first, there are a few fallacies in Yellen’s statement. Industrial output is collapsing, as shown in the PMI index at 52.8 down from 53 in June this is the lowest number since June of 2020. https://www.ismworld.org/globalassets/pub/research-and-surveys/rob/pmi/rob202208pmi.pdf

Keep in mid the Budget was not reduced, the trillions of dollars that was injected into the economy during the pandemic in 2020-2021 expired. It was not done by cost cutting. This means that there is a reduction of spending by both consumers and the government. So, that massive flood of deficit spending is what drove the surge in economic growth in 2021. Now the reduction of the deficit will contribute to building recessionary pressures. The deficit is just reverting to its long-term linear trend.

Lastly, health care costs and housing, have contributed to inflation pressures, (remember all those who chose not to pay rent) but the real pressure is in the daily living costs of Americans. Healthcare and housing, or rent, are fixed for most Americans through contractual agreements. Food, energy, and everything Americans purchase daily are what is sapping their disposable incomes.

While Ms. Yellen may believe there is no recession risk, there are two indicators that currently contradict this. 1) we have had 2 negative quarters of GDP growth. Historically when this has happened a recession has occurred 100% of the time. But let’s not use this metric since there is always a chance of an anomaly. Let’s look at manufacturing production it is declining. While it is true unemployment is low, we have this phenomenon in a shrinking economy because the workforce has shrunk. Lastly the yield curve (10 y and 2 yr Treasury has inverted) this has also been an indicator as to the weakness of the economy. While Yellen may not put much weight into this last piece, to say we see no signs of a recession is an inaccurate statement.

Employment Anomaly

Something does not add up with the jobs report from last week. Perhaps we are entering a new economic paradigm. The extraordinarily strong July Payroll data appears out of sync with all the other incoming data on the state of the labor market. For example, the +30K rise in manufacturing payrolls is at odds with the contraction in the Purchasing Managers’ ISM Manufacturing Index; the +32K rise in construction employment makes little sense when we have seen significant decline in New Home Sales and Single-Family Housing starts; and the rise of +22K in Retail is a head scratcher when Retail Sales volumes are flat to falling, retailers are overstocked, and the likes of Walmart, the U.S.’s largest retailer, are announcing layoffs. Let’s also remember that the Payroll Report is upwardly biased by the birth/death small business automatic add-on, this month we think its likely +100K or more.

Another sister survey, the Household Survey (ignored by the media) did rise +179K in July, mainly from the growth in the number of farm workers. And that +179K still doesn’t make up for the negative -315K June reading. Non-farm employment fell -112K. The Household Survey also reports full-time and part-time jobs, something not shown in the Payroll Repot. Full-time jobs fell -71K in July. All the growth was in part-time work (+250K), not a great statistic that is implying labor market strength.

The official “unemployment rate” (U3 for those with a technical bend), fell from 3.6% to 3.5%, mainly due to another reduction in the Labor Force Participation Rate (LFPR), i.e., the number of people with jobs plus those actually seeking employment. Once again, it is hard to reconcile the fall in the LFPR with the plethora of articles and surveys indicating that many of those who “early retired” during the pandemic have now rejoined the labor force since their portfolios declined. In one survey, 65% of those returning to work said it was because of inflation, while 45% said it was due to the “Bear Market” in equities. In addition, we have seen reports that women with small children have also rejoined as day-care facilities have been re-opening.

Other employment data

The weekly Initial Unemployment Claims (ICs) continue to rise, up +260K the week ending July 30, rising +6K from the prior week and +94K from last spring’s low.

Challenger Gray and Christmas a placement company, that follows layoff announcements, says job cuts are up +36% Y/Y; the June and July totals have increased more than +58K, the highest two month total since February-March 2021.

The JOLTS (Job Openings and Labor Turnover Survey), a favorite of Fed Chair Powell, showed -605K job openings in June (latest data) with job openings down -343K in retail (a record plunge), -91K in leisure/hospitality (down three of the last four months), -21K in manufacturing (after -201K in May) and -71K in construction.

The latest Payroll Report does not change our Recession view! This single data point (the Payroll Report’s +528K), outlier that it is, is playing into the hands of the “no recession” crowd; and we wonder if there isn’t some political pressure here. Based on this single number, markets now think that the Fed will raise rates another 75 bps at their September meeting. There is still a month and a half before the Fed meets again with one more employment story and two more inflation reports in the interim that they will have to digest.

The incoming non-employment data still remains weak:

Residential Construction fell -1.6% M/M in June, the fastest decline since early in the pandemic (April 2020)

Single-Family Construction: -3.1% (June); Pulte, a major U.S. homebuilder, said that orders for new homes fare down -23% Y/Y.

Non-Residential Construction: -0.5% M/M June; -0.8% M/M May. This was broad-based with the Power, Accommodation, Transportation, Highway/Street, and Commercial sectors all negative. (Telecom and Water Supply were positive.)

In a recent New York Times article July 30: Retailer’s Dark Side: As Inventory Piles Up, Liquidation Warehouses Are Busy… To Clear Shelves, Retailers are Selling to Liquidators at Steep Discounts.

Financial Times July 30: “We’ve Never Seen Anything Like This:” U.S. Retailers Compete to Clear Stock.

University of Michigan Survey of Expectations: We have discussed the U of M’s Consumer Sentiment Index in previous articles and its recent probing of historic lows. As part of its process, the survey also inquires as to future expectations. When businesses are downbeat, they cut costs, reduce inventory, slow hiring, and prepare for Recession.

Here is the trend in this index: April: 62.5; May: 55.2; June: 47.5; July: 47.3. June and July data are lower than they were in any of the months just prior to previous recessions which was 49.2 in June of 2008, 50.9 in October of 1990 in September of 2001 the index was 73.5

The recent run-up in credit card debt is also a concern. No doubt consumers are just trying to maintain their standard of living. But credit balances can only rise so far before financial institutions say “enough.” A recent study by the New York Regional Fed indicated that “…the 13% cumulative increase in credit card balances since Q2, 2021 represents the largest increase in more than 20 years.”

Not only is the U.S. consumer showing strains, but so are the consumers in the world’s other major economies.

Whether you buy into the recession narrative or not, businesses all over the country are preparing for a recession. Productivity is down and companies are going to begin reducing expenses, right sizing payroll dumping inventories at steep discounts. So, while many will argue a recession is not imminent being cautious and preparing will not cause you any harm. Source Economist Bob Barone Ph’D

Technical Perspective

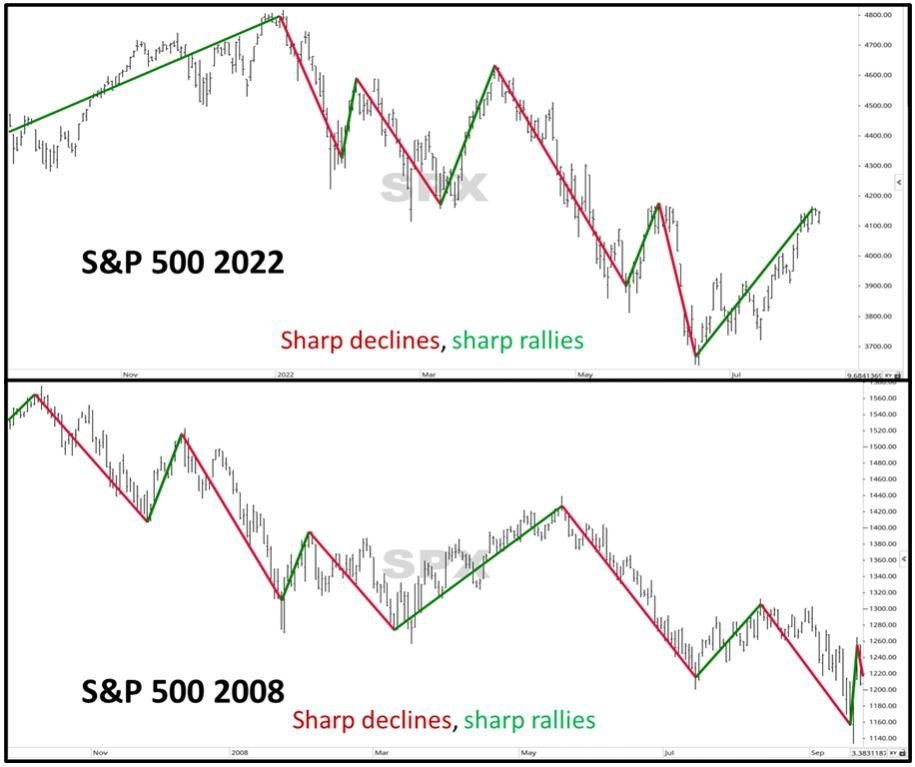

In all market environments, either bull or bear, one thing that is important to avoid is getting “locked in” to a particular position. You may hear many analysts discuss whether they are bullish or bearish and whether the market is right or wrong based on where it is today. But the market is always right regardless. Markets are dynamic, unpredictable, and most importantly, never wrong.

In other words, the “market is where it is,” but you, as an investor, can be right or wrong on your prediction about the market. Which is why you should practice “adaptive portfolio management.” Rather than focusing on where the market may or may not go, focus on reality and adapt your portfolio to deal with current market conditions-- not ones that may or may not exist in the future. For many that have embraced Modern Portfolio Theory or been sold into that investing philosophy is a primary reason why so many retirees had to reenter the work force like we witness in 2008 and are seeing now in 2022.

We discussed a few negative developments in the markets last week, such as high volatility remaining, and the markets being overbought. For this update, there is a short list of positives in the markets. That being said, the market is still bearish. Remember, true bear markets (the ones that take years to get back to a new market high) are full of both declines as well as substantial rallies.

Some Positives:

The S&P 500 is now in what we refer to as Market State 9. Market State 9 is characterized by having cautionary volatility and positive short-term supply and demand indicators. With the recent market rally off the June lows, volatility has fallen off of its highs, but still remains irrational. Also with the rally, short-term indicators have turned positive. This is an improvement for the markets, but one that could easily revert.

We noted last week that the Nasdaq was leading the market’s rally. That is still true, but small caps are also leading large caps. When the markets go up, particularly during volatile markets, we would like to see small cap stocks outperform the larger named securities. A rising ride should lift all ships, rather than having the large boats pull away while the majority of the fleet drowns.

Right now, the market has some short-term resistance, and while it has not yet broken above that resistance level, it has also not bounced off and headed south just yet. The market recently filled two gap downs, which is a positive, and has been hovering around the short-term resistance line for a little over a week now, waiting to make a move one way or the other.

Wide-swinging, volatile markets yield high emotions, on both ends. Investors are optimistic at the peak of a rally, before the market heads lower, and most pessimistic at the market lows before it heads higher.

Some people believe that any modern bear market (which is defined traditionally as -20% drop from a peak) would correct itself much faster because of all the algorithms and technology that exist today, which did not exist 10+ years ago. While this may be true people are still very emotional about money

so while technology has evolved people are still emotional about their investments and while markets are driven by supply and demand, by the emotions, beliefs, and feelings of investors of drive those decisions.

A bear market is traditionally defined as a peak to trough decline of at least -20%. Prior to 2022, the most recent example of a -20% decline was the market events caused by covid. We all know the story: the S&P 500 fell -34% and then rebounded to put in a new high before the year was over. It was one, giant, emotional downturn followed by an equally emotional rally to a new high. That is not a bear market, that is a trading anomaly. All we want to express is to be cautious and be flexible enough to adapt when necessary. Source Brando Bischoff

The Week Ahead

Expectations for another 75bps rate hike in September jumped to a 70% probability after Friday’s jobs report, but the Fed will have another monthly labor report plus two additional inflation readings to consider between now and then. The first of those CPI releases comes this week on Wednesday, and last month’s weakness in commodity prices suggests that headline inflation may have peaked. July’s producer prices follow on Thursday and are also expected to come down given the declines in recent prices paid data. Fed speakers have yet to pivot, so inflation remains the singular focus. Quarterly production figures, Treasury auctions, and consumer sentiment fill out the U.S. calendar. Overseas, preliminary Q2 GDP for the UK will be released on Friday in the aftermath of the BOE’s gloomy forecast and the pound’s steady downtrend. In Asia, China announces inflation numbers late Tuesday amid concerns of the property crisis spilling over into the highly leveraged banking sector.

This article is provided by Gene Witt of FourStar Wealth Advisors, LLC (“FourStar” or the “Firm”) for general informational purposes only. This information is not considered to be an offer to buy or sell any securities or investments. Investing involves the risk of loss and investors should be prepared to bear potential losses. Investments should only be made after thorough review with your investment advisor, considering all factors including personal goals, needs and risk tolerance. FourStar is a SEC registered investment adviser that maintains a principal place of business in the State of Illinois. The Firm may only transact business in those states in which it is notice filed or qualifies for a corresponding exemption from such requirements. For information about FourStar’s registration status and business operations, please consult the Firm’s Form ADV disclosure documents, the most recent versions of which are available on the SEC’s Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov/

The Optimized Investor