Could we be in the Eye of the Storm

Weekly Market Review for March 31st, 2023

The content of this Newsletter is to provide you with Economic insights to assist you in making better decisions with your investments. Unlike many other financial periodicals we will not mention specific companies, unless it is relevant to an overall economic issue. We welcome your questions on economic concerns and will address in our newsletter. just email us at info@optfinancialstrategies.com #FinancialAdvisor,#investmentmanagement #wealthmanagement #financialplanning #retirementplanning #401kplans

Week In Review

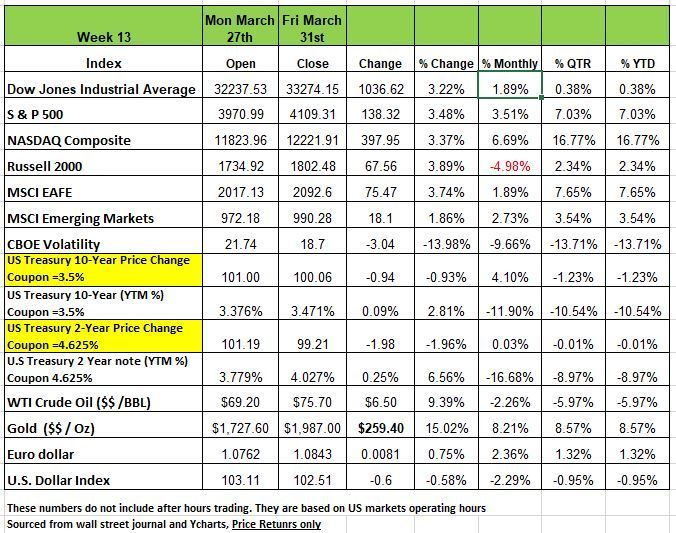

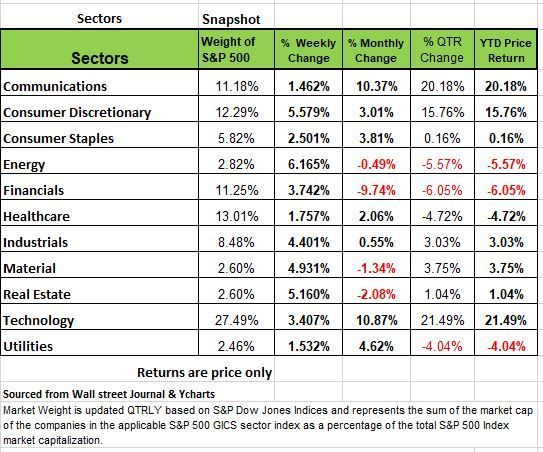

Friday market the end of the trading week, Month and first Quarter of 2023. All 4 of the major indices were up this week with the DOW posting a +3.22% increase for the week,1.89% increase for the month and .38% for the quarter. The NASDAQ led the pack by posting a +16.77% return for the first 3 months of 2023. This was led by the technology sector which is up +21.49% so far this year. The S&P 500, the market Benchmark was up +3.48% for the week and bring the first quarter return to +7.03%. The Russell 2000had the largest weekly increase at +3.89% but was down for the month -4.98% bringing the Q1 return in at +2.34%. Much of the trauma in the small cap sector ell was caused by the collapse of smaller regional banks Silicon Valley Bank (SVB)and Signature Bank (SBNY). Confidence was restored Monday when First Citizens Bancshares (FCNCA) agreed to acquire the former assets of SVB, which was amplified by the likelihood that the Fed would expand its emergency lending facility. The financial sector added another 3.7% to the previous week's 0.5% gain.

The energy sector was the top-performing sector of the S&P 500 with a gain of 6.2%. Fueled by higher oil prices on heightened geopolitical tensions tied to overtures by Russia to place nuclear weapons in Belarus and Iraq's suspension of exports from the Kurdistan region. In addition, OPEC announced over the weekend that it would cut production so expect this sector to increase on that news

Material stocks were higher by 4.9%, followed by a 4.4% gain in the industrial sector with the airlines all grabbing the top spots. Airline industry research underpinned the sector with forecasts for active summer travel and higher airline fares.

The real estate sector rose another 5.2% this week led by gains in Boston Properties (BXP) and Simon Properties (SPG) while consumer discretionary was up 5.6% from outsized gains in Caesars Entertainment (CZR) and Carnival (CCL), with Carnival gaining an upgrade by Susquehanna to positive from neutral.

Consumer staples closed the week 2.5% higher, followed by a 1.8% gain in healthcare stocks. Communication services ended with a 1.5% gain as losses in Google (GOOG) were offset by a 10% gain in Paramount (PARA).

Consumer confidence improved, fourth quarter GDP was revised slightly lower, and a key inflation metric for the Federal Reserve, the PCE deflator, rose less than expected last month, mitigating forecasts for rate increases.

U.S. Treasury Bond yields were up across the yield curve last week as market tensions over the banking sector appeared to have simmered. All eyes were on economic data reported at the back half of the week. On Thursday, real fourth quarter GDP was revised lower to 2.6% from a prior estimate and consensus expected 2.7% annual rate. Contributions came from inventories, consumer spending, and government purchases. While home building corporate profits weighed on GDP. The PCE deflator, the Federal Reserve’s preferred inflation indicator, rose 0.3% in February and is up 5.0% versus last year. Friday’s inflation data indicated that despite the recent banking turmoil, the Federal Reserve still has work to do to combat inflation.

Eye of the Storm

If you think the financial challenges are behind us, you may want to rethink your basis for believing we are in the clear. It’s very rare that major shock to a system will result in a one-off event. If we look back to April of 2007 subprime lender New Century Financial filed for bankruptcy, New Century was just the first a year later Bear Sterns announced it had liquidity issue, so the Fed gave them a line of credit, which did not help very much, and the company was forced to sell to JP Morgan for pennies on the dollar. You know what happened after that with Lehman Brothers and the housing market.

While the past week brought some calm to the financial sector because no other banks had cash outflow issues and stock prices stopped falling, it appears that we may just be in the “eye of the storm”. While the Fed has given banks a liquidity lifeline, keep in mind it is temporary, not a permanent fix. If interest rates continue to rise consumers will be pulling more money out of low interest accounts and placing, it in higher interest-bearing vehicles. But this is not where the problem lies, we have multiple issues pending and the only question is when the dominos will start falling.

The liquidity issue is impacting the commercial real estate market. With Defaults and vacancies on the rise at high-end office buildings, another sign that remote work and rising interest rates are spreading pain to market segment. Banks are holding approximately $3 trillion in commercial real estate paper. In addition, there are a large number of companies that hold debt for REITS, which also include mortgages on these buildings.

Until the SVB debacle, smaller banks did a better job of keeping their deposit base than larger banks. So, now the Fed has given banks a temporary liquidity lifeline. But that’s a temporary fix – it doesn’t solve the issue! So, it is likely that something else is going to break. The Fed appears to be caught between a rock and a hard place. On the one hand, despite evidence of falling inflation, it believes it must maintain its credibility in its inflation fight by raising interest rates. On the other hand, it is providing a huge amount of liquidity (cash) to restore confidence in the banking system. But this provision conflicts with the objective of taming inflation

The liquidity issues seem destined to make the Recession both deeper and longer. Below are some points as to why we think this way.

Banks hold $3 trillion of Commercial Real Estate (CRE) loans, the largest loan category on their balance sheets and nearly doubling in size since the Financial Crisis in 2007.

Defaults and vacancies are on the rise at high-end office buildings, in the latest sign that remote work and rising interest rates are spreading pain to more corners of the commercial real-estate market.

Over the past month, we have noted rising foreclosures in this space and the Wall Street Journal posted the following article last week. https://www.wsj.com/articles/distress-in-office-market-spreads-to-high-end-buildings-c1adad48

Banks were already tightening lending standards prior to the financial chaos created by SVB and the liquidity issues and questions revolving around the value of their bonds and loans, they really have no choice but to increase their balance sheets. This means even tighter lending standards, making borrowing more difficult and much more expensive, all at a time when corporations have been limiting their capex plans. This is not a positive picture for economic growth.

Another issue, both for the banks and the economy in general, is the accelerating fall in home prices. As you can see from the table that Residential Real Estate is nearly a quarter of bank loans. The Case-Shiller Home Price Index fell again in January (-0.4% M/M; latest data) and this index has been falling for seven months in a row. Over that period, the annualized rate of contraction is -7.5%.

The largest asset consumers have on their balance sheets is their home. It is used to finance everything from vacations to college education. Right now, homes in the U.S. are worth approximately $48 trillion. In 2007, that number was $26 trillion, so quite the increase in just 16 years. Over the last three years, home prices have risen +36%, so logically we can expect some price reversion as the Recession unfolds. For example, if home prices were to fall by -25%, that would wipe out $12 trillion of homeowner equity likely to elicit a large negative wealth effect, perhaps reducing consumption by -5%.

If home prices fall by that -25% number, or even less, some recent purchasers of homes that overpaid for homes during the pandemic in a rush to leave the cities have a high probability of finding themselves with negative equity. This is similar to what happened back in 2008. If unemployment rises the loss of a job in these household will likely result in non-payment and eventual foreclosure, with the mortgage holder eating the loss.

Then we have the ever present “Zombie” company The Walking Dead of both private and publicly traded companies. While Zombies are fictious they are all too real in the business world. A zombie company is one that struggles to service its debt or a bank that is technically insolvent but avoids collapse. They started to evolve in the last decade during the era of easy money that the US Federal Reserve and other central banks started to address the crisis in 2008. Debt was cheap and money was in abundance, so these companies had access to cash at all times and did not have to pay attention to efficient operations for profitability. More zombie companies are popping up. Tighter money and stricter lending requirements in addition to the cost of borrowing now threatens to create more unfit companies that were barely holding on when money was cheap. Central bankers will face tricky balancing acts as they try to cool inflation without creating more of these worthless companies. One way to identify these companies is to look at their balance sheets and see how many have over borrowed. https://www.bloomberg.com/news/articles/2023-04-01/zombies-are-back-here-s-why-that-s-economic-trouble-quicktake

Lastly of course, there are those consumers, credit card, and auto loans. As we have discussed in prior blogs, delinquency rates for those categories are already on the rise.

We bring this up not to scare you but to inform you so that you may take measures to protect your portfolio from the downside. As we have addressed in the past, having a portfolio on autopilot is not wise when entering a challenging economic period. Active management is wiser especially if you are entering the final stage of your work career. While interest rates are up and you can make a decent yield in money market mutual funds, you also do not want to be 100% in cash as you can go broke just waiting for Armageddon.

Sources Economist Bob Barone Ph’D

The Week Ahead

A shortened week lies ahead, with U.S. markets closed Friday in observance of Good Friday. But the latest batch of U.S. jobs data will give investors plenty to consider, starting with JOLTS job openings on Tuesday, followed by ADP private payrolls on Wednesday, and most importantly the monthly government employment report on Friday.

The U.S. economy is expected to have added another 240K jobs in March, further supporting the idea that interest rates will have to stay higher for longer despite recent financial stability concerns.

This week delivers ISM PMIs, and the red-hot services sector has been adding to inflationary pressures while manufacturing languishes. U.S. factory orders are also on the domestic calendar. Overseas, OPEC+ meets today and is unlikely to tweak its policy, sticking to production cuts enacted in November. Later today the Reserve Bank of Australia meets, with the possibility of a pause in the rate-hiking cycle after inflation slowed in February. Germany’s factory orders and industrial production highlight the European docket.

This article is provided by Gene Witt of FourStar Wealth Advisors, LLC (“FourStar” or the “Firm”) for general informational purposes only. This information is not considered to be an offer to buy or sell any securities or investments. Investing involves the risk of loss and investors should be prepared to bear potential losses. Investments should only be made after thorough review with your investment advisor, considering all factors including personal goals, needs and risk tolerance. FourStar is a SEC registered investment adviser that maintains a principal place of business in the State of Illinois. The Firm may only transact business in those states in which it is notice filed or qualifies for a corresponding exemption from such requirements. For information about FourStar’s registration status and business operations, please consult the Firm’s Form ADV disclosure documents, the most recent versions of which are available on the SEC’s Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov/

The Optimized Investor