The Persian Pivot – A Conflict of Attrition Analyzing the Iranian Escalation and the "Long War" Trap

Newsletter

Week Ending February 27th 2026

Market Recap

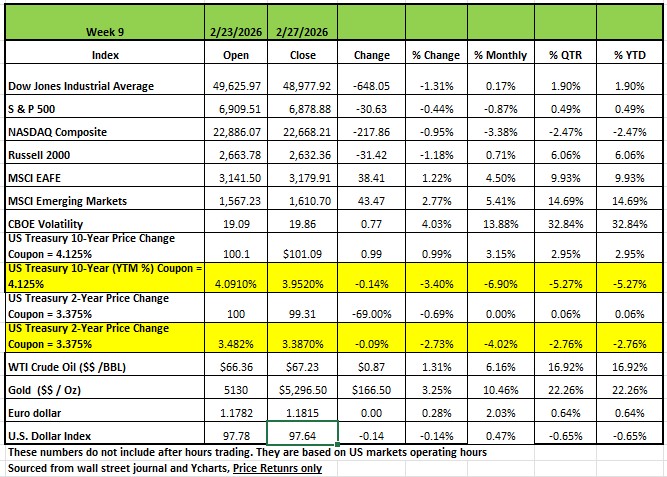

All four of the major indices were down last week, which also ended February trading. The Largest decline was in the DOW -1.31% followed by the Russell 2000 -1.19% the NASDAQ -0.95% and the S&P 500 -0.44% . The NASDAQ ended the month down -3.38%. The S&P 500 decline last week, was led by the technology and financial sectors. The index ended the month down -0.87%.

In economic news, the US producer price index rose by 0.5% in January following a 0.4% increase in December, according to the Bureau of Labor Statistics. This was higher than the 0.3% gain expected in a Bloomberg survey.

After excluding the more volatile food and energy prices, core PPI rose by 0.8%, higher than the 0.3% gain anticipated and the previous month's 0.6% jump.

A blizzard hit the East Coast on Monday, causing delays and cancellation by airlines and other travel companies. Utilities proved to be the best performing sector, led by Constellation Energy’s + 11.88% return after reported earnings impressed analysts. Other defensive sectors Consumer Staples +2.71% and health care +2.14% came in second and third place, respectively. The information technology sector performed worst among sectors -2.18%, with semiconductor names NVIDIA and Broadcom being the two most negative individual contributors to the S&P 500’s return, returning -6.65% and -3.94%, respectively. NVIDIA announced strong earnings that exceeded analyst expectations, but Michael Burry of “Big Short” fame in a blog post on Thursday warned of risks to the chip giant if its non-cancellable purchase orders meet a significant slowdown in the AI industry. The financials sector was the second worst performer -1.95% as Citrini Research released a report on Monday outlining potential AI risks to existing jobs and industries that sent payment names such as American Express lower (-10.77%); large banks such as JPMorgan Chase and Wells Fargo fell -3.28% and -8.17%, respectively. Turning to economic news, factory orders for December fell -1.4%, in line with expectations.

Treasury yields declined across the board, with longer-duration yields falling more than shorter-duration yields. The 10-year Treasury note fell below 4% for the first time since November as geopolitical tensions, tariff uncertainty, and fears of AI disruption have triggered a flight-to-quality. Following the Supreme Court’s decision last week to strike down President Trump’s tariff program, he signed an executive order imposing a new 10% global tariff on most imported goods, which took effect on Tuesday. On Friday, President Trump said that he was “not happy” with the progress of negotiations with Iran over its nuclear program and threatened military action, which was executed on Saturday with coordinated efforts by Israel, killing Iran’s supreme leader Ayatollah Ali Khamenei. Iran retaliated by attacking neighboring countries Israel, Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates (UAE). The US now has the largest US military build-up in the Middle East since the invasion of Iraq in 2003.

Also on Friday, the January Producer Price Index (PPI) rose 0.5%, beating the consensus expected 0.3%. Despite the outsized monthly reading, producer prices have moderated on a year-ago basis and are up 2.9% versus January 2025.

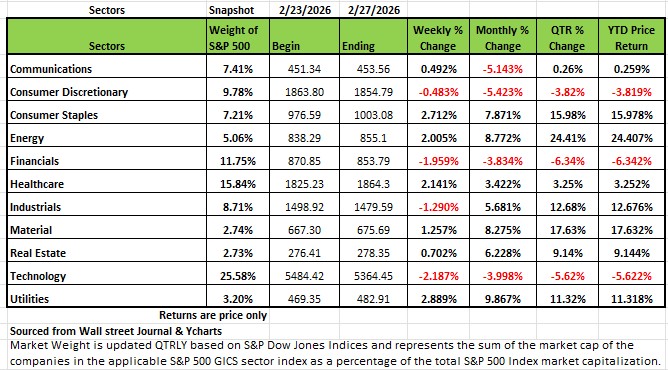

By Sector

The technology sector had the largest percentage drop of the week, falling -2.18%, followed by a -2% decline in Financials and a -0.5% loss in Consumer Discretionary. Industrials also edged lower-1.29%.

First Solar (FSLR) was hit hardest in technology, sliding 18% as the company posted Q4 earnings per share below analysts' mean estimate despite higher-than-expected net sales. First Solar also forecast 2026 net sales below the Street view at the time.

International Business Machines (IBM) shares also weighed on the technology sector, falling -6.6%. Morgan Stanley analysts said the company faces "some degree" of artificial intelligence disruption risk due to recent innovations with generative AI.

KKR (KKR) and Apollo Global Management (APO) had the largest percentage drops in the financial sector for the week, falling -13% each.

On the upside, utilities rose 2.9%, followed by a 2.7% increase in consumer staples, a 2.1% gain in health care and a 2% rise in energy. Materials, real estate and communication services also edged higher.

Constellation Energy (CEG) had the largest percentage increase in utilities, climbing 12% as the company reported Q4 adjusted earnings per share and operating revenue above analysts' mean estimates.

In consumer staples, shares of J.M. Smucker (SJM) rose 5.1%. The food producer trimmed the top end of its full-year sales growth outlook due to a recent fire at one of its manufacturing facilities, but its fiscal third-quarter results topped market estimates.

This week, CrowdStrike Holdings (CRWD), Broadcom (AVGO), Costco Wholesale (COST) & Best Buy (BBY) are among the companies scheduled to release quarterly results.

On the economic calendar, February auto sales are expected on Monday, while the month's payrolls and unemployment are set to be released on Friday.

The Persian Pivot – A Conflict of Attrition

Analyzing the Iranian Escalation and the "Long War" Trap

The geopolitical landscape was fundamentally rewritten this past weekend. Following the joint U.S.-Israeli Operation to strike Iran. A massive strike targeted Iranian command centers and missile sites, took out its supreme leader Ayatollah Ali Khamenei along with most of its political and military leadership. Now the global economy is now bracing for a "long war" scenario. For most investors, the critical focus has shifted from the shock of the attack to the structural endurance of the combatants and the cascading fallout across global markets.

The Immediate Shock: Energy and Logistics Paralysis

The most direct economic consequence has been the immediate seizure of the world’s most critical maritime chokepoint. Iran has effectively closed the Strait of Hormuz, removing roughly 20 million barrels of oil per day (one-fifth of global consumption) from the market. Ships are not able to get insurance since the attack and crews run the risk of losing their life from attacks by Iran creaking a bottleneck

Brent crude spiked 10% on Monday morning to $82 per barrel, with some forecasting a price of $100+ if the blockade persists for several days. This will translate into a massive "inflation tax," and most likely derail the Federal Reserve’s "soft landing" and forcing the ECB to pause its planned rate cuts.

The conflict has already put logistics in turmoil. Major shipping lines like Maersk are rerouting around the Cape of Good Hope, adding 10–15 days on transit and roughly $1 million in fuel costs per voyage. Additionally, the closure of UAE and Qatari airspace has severed the primary aviation corridor between the West and Asia, sending air freight rates up by 400%.

Iran’s Economic "Death Spiral"

Tehran’s decision to engage in high-intensity conflict comes at a moment of extreme domestic fragility. The regime is operating with almost no fiscal cushion. In addition, the Iranian Rial has plummeted to record lows, exceeding 1,000,000 IRR per USD in unofficial markets. Defense spending hiked by 145% in nominal terms, but with inflation exceeding 50%, the military is cannibalizing the civilian economy. While Iran can maintain "nuisance" warfare (using $20,000 drones to force the U.S. to expend multi-million-dollar interceptors) it lacks the industrial base to sustain a high-intensity conventional war for 12 months without risking total state failure or a “bread riot” revolution. The Iranian people are already angry with the recent killings of protesters and much of the country has struggled economically from sanctions

The U.S. Readiness Gap: Attrition and Personnel

The U.S has its own set of challenges with this conflict. A prolonged conflict (one exceeding 4–6 weeks) exposes two critical vulnerabilities for America: munitions exhaustion and manpower shortages.

The Munitions Gap

The U.S. is currently winning the tactical battles but losing the "expensive math" of attrition. Some reports indicate the U.S. Navy has expended SM-3 and SM-6 interceptors at an unsustainable rate. In 2025 alone, a previous skirmish between Israel and Iran the U.S. consumed 25% of the total THAAD stockpile in 12 days. We will continue to deplete our inventory in a prolonged conflict. Replacing high-end munitions like the "Bunker Buster" GBU-57 takes years, not months to replenish. A year-long war could leave the U.S. "archers without arrows" if another conflict evolves, like the Taiwan Strait.

There is also a Personnel Crisis occurring in the U.S. military, The military has missed its recruiting targets in 2025, so the U.S. military remains "short-handed". Only 23% of American youth currently meet physical and academic standards for service. This alone presents a problem for the U.S. military both in the long run and the short term. A "long war" requires rapid rotations. With the force already understrength, the high operational tempo (OPTEMPO) risks a retention crisis among experienced NCOs which is the backbone of the military’s combat effectiveness.

Then we have the budgetary issues. The U.S. Debt is already higher than our GDP, and these munitions don’t come cheap. The dollars needed to produce arms and recruit personnel will cost taxpayers.

The Bottom Line

We are entering a period of strategic attrition. While the U.S. and Israel possess overwhelming technological superiority, Iran is betting that it can outlast the Western appetite for high energy prices and the depletion of expensive missile stockpiles. For investors, the "geopolitical risk premium" is no longer a temporary spike; it is a structural feature of the 2026 market. Volatility will continue.

The Week Ahead