Riding the Wave of Volatility

This article is provided by Gene Witt of Optimized Capital LLC. for general informational purposes only. This is an opinion, not investment advice. This information is not considered an offer to buy or sell any securities or investments, nor is it considered investment advice. Investing involves the risk of loss, and investors should be prepared to bear potential losses. Investments should only be made after a thorough review with your investment advisor, considering all factors, including personal goals, needs, and risk tolerance. Optimized Capital Registered Investment Adviser (RIA) that maintains a principal place of business in the State of Illinois and Indiana. The Firm may only transact business in those states in which it is notice filed or qualifies for a corresponding exemption from such requirements.

Market Recap

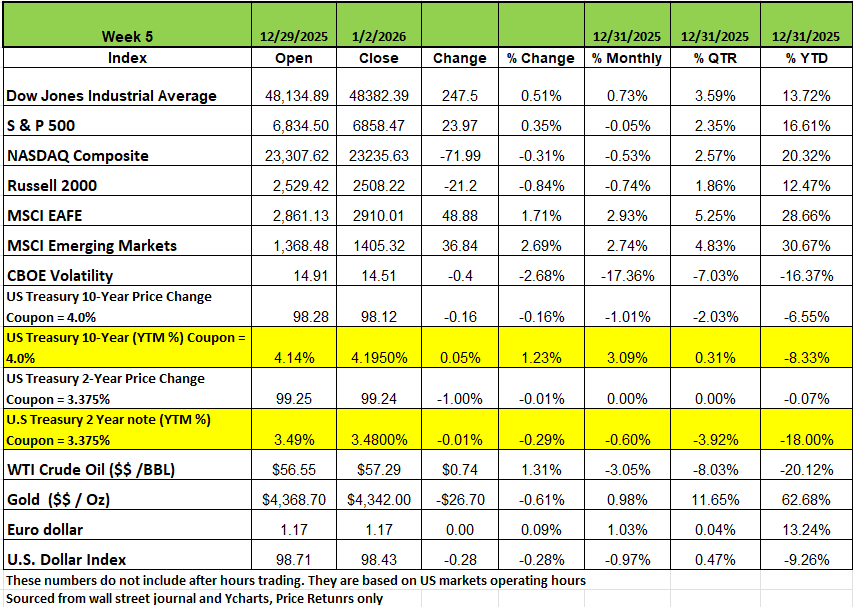

2025 came to an end last week and we enjoyed another year of all four of the major indices posting excellent returns. The NASDAQ posted the largest gain on the year with a +20.3% increase, followed by the S&P 500 with a + 16.6% return, the DOW +13.72% and the Russell 2000 +12.47%. This would be the 3rd year that all indices posted double digit returns. A handful of companies saw tremendous returns in 2025 like Newmont Corp (NEM) posting a +168% return thanks to the price of gold soaring. A few technology companies such as Western digital (WDC), Micron (MU) and Seagate Technology (STX) posted returns of greater than 200%. But keep in mind that more than 40% of the companies in the S&P 500 experienced negative returns in 2025.

Treasury yields ended the holiday-shortened week mixed, as shorter-duration yields were mostly lower while longer duration yields edged higher. The 10 yr Treasury started the year with a coupon of 4.25% selling at a premium and ended the year with a 4% coupon selling at a discount. The 2 yr Treasury began 2025 with a coupon of 4.25% and ended with a coupon of 3.375%, almost a full percentage point lower.

Initial jobless claims fell to 199,000 for the week ending December 27, a 16,000 decrease from the previous week’s revised level of 215,000. Gold prices fell sharply after ending last week at an all-time high, breaking a three-week winning streak. Despite the decline, gold was one of the best-performing assets in 2025 and posted its best annual performance since 1979. Oil futures finished the week higher despite falling the last three days of the week. Concerns about an oversupply of oil have been partially contained by geopolitical risks, as the Russia-Ukraine war continues, and tensions rise in the Middle East.

Next week's US economic data will include December automotive sales as well as the Institute for Supply Management's December manufacturing index on Monday. The Institute for Supply Management will also release its December services index on Wednesday. Finally, the government's closely followed December employment report will be released on Friday

By Sector

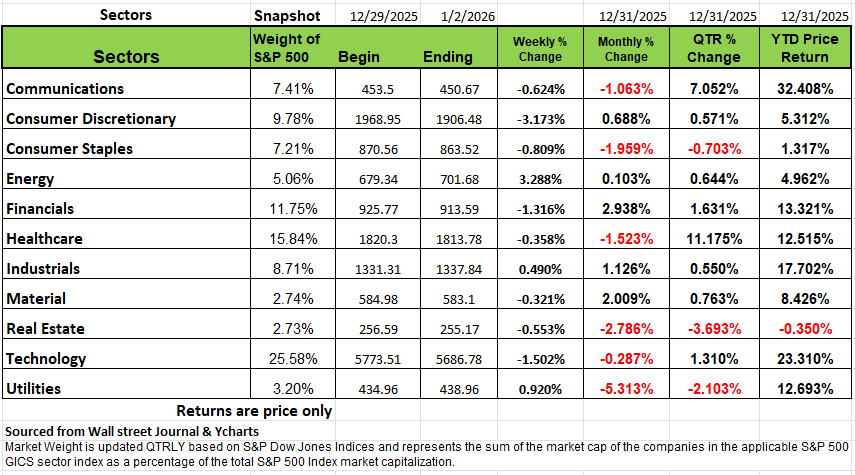

Ten of the 11 sectors in S&P posted positive numbers in 2026 with Real Estate -0.35% still struggling since the pandemic. The largest Sector gain in 2025 was communications with a +32.4% return followed by information technology with a +23.3% gain. Industrials followed with a +17.7% return, Financials +13.3% Healthcare and Utilities both with more than a +12.5% return. Materials posted a return of +8.4%, Consumer Discretionary + 5.3% Energy +4.9% & Consumer Staples +1.3%. Consumer Discretionary may be showing signs of weakening consumer as spending has dropped significantly. But what else can you expect after the government deployed $5 trillion into the economy during the pandemic.

In the Communications Sector Warner Brothers posted the highest return with a +172% on the bidding war between Netflix and the new Paramount Skydance company. Google was the next best performing stock in the Sector with a +65% gain the two biggest losers in the Sector were Charter Communications -39% and Comcast-14.9%

In the Consumer Discretionary Sector Tapestry posted the largest gain with a +95.58% increase, followed by Ralph Lauren +53.09% GM +52.66%, Expedia +52.05%, the largest declines in this sector were, CarMax -52.74%, Decker Outdoors -48.95% and Lululemon -45.66

Consumer Staples Sector was led by Dollar General +75.11, followed by Dollar Tree +64.1% and Monster Beverage +45.87%, the Decliners in the Consumer Staples Sector were Clorox -37.9%, Conagra -37.6% and Constellation Brands -37.5%. It appears that drinking alcohol is not in Vogue so much with the Gen Z crowd.

Energy Sector was led by Valero Energy +32.7%, Marathon +16.5% and EQT Corporation +16.2% The losers in the Energy Sector were, Oneok -26.79% Texas Pacific Land Corporation -22.09% and Occidental Petroleum-16.78% (one of Warren Buffets favorite companies)

In the Financial Sector, Citibank led the way with a +65.78% gain, Goldman Sachs +53.5% and The Bank of New York Mellon Corp +51.1%. Fiserv the financial transaction company was down -67.3% followed by Factset -39.58% and PayPal -31.6%

Healthcare Sector was led by CVS +76.79%, Cardinal Health +73.75%, and IDEXX Laboratories +63.63% Molina Healthcare -40.37%, Dentsply Sirona -39.7% and United Healthcare all had the largest declines in 2025.

The Industrial Sectors were one of the biggest beneficiaries of the AI movement as Wallstreet looked for ways to power the new data centers. GE Vernova almost double in price in 2025 with a +98.7% increase, followed by Howmet Aerospace +87.46%, & GE Aerospace 84.68%.The companies with the largest declines were Copart -31.7%, Builder First Choice-28.% & Carrier Global -22.59%

Materials Sector was led by Newmont (a gold miner) +168.7% Albemarle Corp +64.31% and Steel Dynamics +48.55%. FMC Corp price declined -71.4%, Dow -41.74% & LyondellBasell Industries -41.7%

The Real Estate Sector did have some winners Welltower +47.27%, Ventas +31.4% and CBRE+22.4% on the downside Alexandria Real AEstate -49.8%, Iron Mountain -21.08% & Healthpeak Properties -20.67%

The Technology Sector had some significant gains by some of the companies in this sector such as Micron Technologies posting a +239.1% gain followed by Seagate Technology +219.07%, and Western Digital +188.9%. The companies that did poorly in this sector were, Enphase Energy -53.3% and Gartner -47.93% and GoDaddy -37.13%

Lastly the Utilities Sector saw NRG Energy +76.5%, followed by Constellation Energy +57.9% and American Electric Power +25.02%. only 3 companies in this sector saw their price drop, Edison International – 24.82% PG&E -20.37% and Public Service Enterprise -4.95%

Riding the Wave of Volatility

If 2025 taught us anything, it’s that "normal" is a relative term in the stock market. We’ve seen a year where VIX (the market's "volatility gauge") felt like a heart monitor, spiking on policy shifts and calming on corporate earnings. The Vix ranged form a high of 60.13 to a low of 13.38. That is quite a spread. As we look toward 2026, the question isn't whether there will be volatility—but perhaps the size of the next wave and where it will come from.

2025: The Year of the "Policy Shock

2025 was defined by instability over uncertainty. We felt the concern when the markets plunged on April 7th “Liberation Day”. The S&P 500 and the DOW both declined by more than 10% from the Jan 1st levels. Fear drove investors to Treasury Bonds causing the yield to drop. However, a day later markets rebounded after the President announced a delay in tariffs.

The AI "Reality Check": Tech valuations were forced into a massive repricing as investors shifted from blind enthusiasm to demanding proof of actual ROI. Companies like Oracle jump nearly $100/share on the September quarterly call and outlook on new business on data centers to be built. However, the high did not last very long when analyst realized just how much money it would take to meet those lofty goals and the stock plunged shortly thereafter.

The Fed Under Fire: 2025 saw unprecedented public friction between the White House and the Federal Reserve over interest rates, keeping bond yields in constant flux and the market listening to every word that Chair Powell used at his press conferences.

The Affordability Crisis: From 2025 Focus to 2026 Reality

In 2025, "affordability" moved from a kitchen-table complaint to the central pillar of U.S. economic policy.

The Boiling Point: Last year, the housing market hit a historic "lock-in" effect. With mortgage rates hovering near 7% for much of the year and home prices reaching all-time highs in June 2025, the income required to buy a median home climbed to over $110,000. This priced out the vast majority of first-time buyers and made "cost of living" the #1 voter concern.

The Slow Thaw: As we enter 2026, we are seeing the first signs of a "normalization." Mortgage rates are finally drifting into the low 6% range, and home price growth is expected to slow to roughly 2.2%.

The "Real" Wage Gap: The big story for 2026 is that wage growth is finally projected to outpace inflation. For the first time since 2022, the typical mortgage payment is expected to slip below the 30% affordability threshold of median income. While it won't feel like an overnight fix, the "affordability squeeze" is transitioning from an acute crisis to a gradual recovery.

If 2025 taught us anything, it’s that "normal" is a relative term in the stock market. However, the first week of 2026 has already delivered a geopolitical "black swan" that has fundamentally shifted the global risk map. As we look at the year ahead, the conversation has moved from domestic policy to a high-stakes global transition.

To start the year off the U.S captured and is prosecuting Venezuelan President Nicolas Maduro. The capture of Maduro over the weekend, during Operation Absolute Resolve, has introduced a massive new variable into the markets. While the administration frames this as a "restoration of order," the market is reacting to the immediate logistical and political consequences.

The Death of the "Rules-Based Order"

The most immediate impact is the erosion of international norms. By sidestepping the UN Security Council to seize a sovereign leader on criminal charges, the U.S. has effectively signaled the end of the "Rules-Based International Order" in favor of a "Spheres of Influence" model.

The Russian View: Paradoxically, Moscow’s response has been one of "grudging respect." While the Kremlin officially condemned the "act of armed aggression," high-ranking Russian officials have noted that this sets a precedent. Putin’s takeaway is a quid pro quo: If the U.S. can exercise total military dominance in its "backyard" (the Western Hemisphere), then Russia is morally and militarily justified in doing the same in its "Slavic sphere" (Ukraine and Eastern Europe).

The Chinese View: Beijing is "deeply shocked," but for a different reason. They view this as a direct threat to their Global Security Initiative, which promises partners that China can protect them from Western intervention without military force. The capture of a "strategic partner" like Maduro proves that Beijing’s security guarantees currently lack the teeth to stop U.S. kinetic action.

The Economic War for Infrastructure

The capture has turned Venezuela into a massive "repo operation" for global debt.

China’s Financial Exposure: China is Venezuela’s largest creditor, with tens of billions in oil-backed loans. Beijing is now terrified that a U.S.-led transition government will prioritize U.S. oil majors and "wipe the slate clean" on Chinese debt. We expect 2026 to be defined by a "Debt vs. Oil" standoff, where China may use its leverage in the G20 to stall any Venezuelan recovery until its loans are guaranteed.

Russia’s Military Loss: Russia has spent two decades and billions of dollars turning Venezuela into its primary military outpost in the Americas. With Maduro in New York, the U.S. now has potential access to advanced Russian hardware—including S-300VM air defense systems and Pantsir missiles—that were delivered as recently as late 2025. This seems to be an intelligence nightmare for Moscow.

The Energy Rebound / Risk

With Maduro in U.S. custody and the administration announcing plans to have U.S. oil companies manage Venezuela's nationalized industry, energy markets are on edge.

The Opportunity: If the U.S. can successfully stabilize Venezuela's production (once peaking at 3.5 million b/d), we could see a long-term downward pressure on oil prices, benefiting global transport and manufacturing.

The Risk: Short-term supply disruptions due to civil unrest in Caracas or sabotage of infrastructure could cause immediate price spikes at the pump. The capture of Maduro has done more than just destabilize the Caribbean; it has fundamentally redrawn the lines of the "Great Power Competition between U.S., China and Russia

Domestically

The Federal Reserve Transition

In May 2026, Jerome Powell’s term as Fed Chair will expire. The market hates a vacuum, and the nomination of a successor—against the backdrop of a potential U.S.-led transition in Venezuela—will be a major volatility trigger. Investors are watching for a Chair who can balance "geopolitical spending" with inflation control. But as we discussed in our December 22 newsletter the voting block of Fed Regional Presidents will rotate in 2026 so a new group will be voting on rates, and much of this group sits on the more hawkish side of where rates should be.

The Investor’s Playbook for 2026

In this high-stakes environment, "buy and hold" requires more stomach than ever.

Energy Sector Selective: Don't just buy "oil." Look at the specific U.S. majors (Chevron, etc.) that already have legacy footprints in Venezuela and are positioned to lead the infrastructure rebuild.

Defense as a Hedge: Given the "Absolute Resolve" posture, aerospace and defense remain a primary hedge against further geopolitical escalations in the region.

Quality Over Growth: With the AI bubble still deflating and geopolitical risks rising, 2026 is a year for "Fortress Balance Sheets"—companies with low debt and high free cash flow.

Focus on Discretionary Spending: As affordability improves and "real" wages rise, look for a rebound in consumer discretionary stocks that were hammered in 2025.

Energy Sector Selective: Watch U.S. energy majors with legacy footprints in Venezuela; they are positioned to lead the infrastructure rebuild.

The Bottom Line: Volatility is not the enemy; it is the market's way of pricing in a rapidly changing world. The capture of Maduro has accelerated a shift toward "geopolitical investing" that will likely define the rest of the decade. It feels like we may be entering a "Cold War 2.0"but will be far more dynamic and action driven than before. For the stock market, this means the "Geopolitical Risk Premium" is no longer a temporary spike; it is a permanent feature of the landscape. Investors should expect increased volatility in companies with high exposure to the South China Sea and those reliant on European security stability

The Week Ahead