The State of Private Credit & Bank Exposure, The Good, the Bad and the Ugly

Weekly Market Newsletter

Week Ending March 13th 2026

Marker Recap

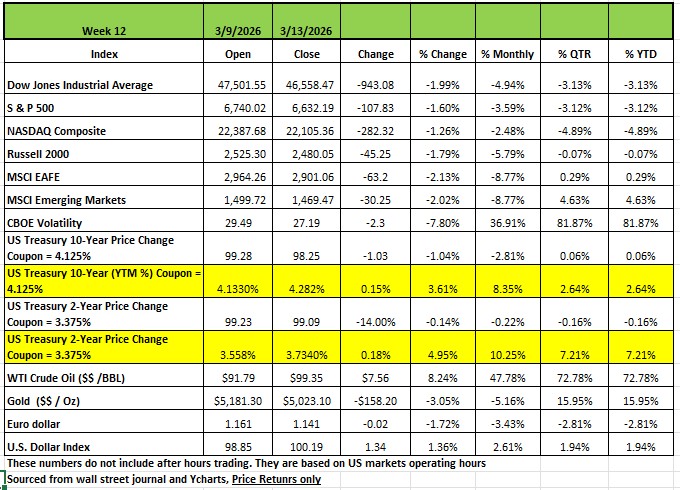

All four of the major indices fell last week, with the DOW posting the largest decline, with a -1.99%. This was followed by the Russell 2000 -1.79% the S&P 500 -1.6% and the NASDAQ -1.26%. Last week’s pullback put all of the indices in the red for the year. It's the third consecutive weekly decline, as oil prices continued to climb amid turmoil in the Middle East. The S&P 500 ended the week at 6,632.19. It is now down -3.6% in March and has fallen -3.1% this year. The NASDAQ is down -2.48% in the month but -4.89% YTD. As the US-Iran war neared the two-week mark, most sectors of the S&P 500 fell. The energy sector bucked the decline as Brent crude, the global benchmark, reached its highest settlement value since August 2022. The climb in crude oil futures came even as the US began allowing countries to buy sanctioned Russian crude already at sea. Adding to investors' concerns, government data showed Q4 gross domestic product was lower than previously estimated amid weaker consumer spending and a larger downturn in exports. The report showed US real gross domestic product came in at a 0.7% annualized growth rate in the December quarter; Wall Street expected growth to match the initial +1.4% estimate, according to a survey compiled by Bloomberg. Economic data will include the February producer price index as well as February industrial production and pending home sales. Also, the Federal Open Market Committee will hold a two-day meeting concluding with a decision on interest rates.

By Sector

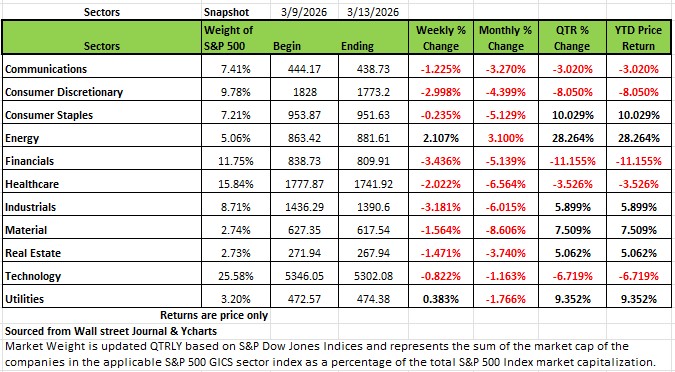

Nine of the 11 sectors were in the red last week with the financial sector posting the largest percentage drop of the week, falling -3.4%, followed by a -3.2% loss in industrials and a -3% decline in consumer discretionary. Health care, materials, real estate, communication services, technology and consumer staples also fell.

Fiserv (FISV) and Global Payments (GPN) were hit hardest in the financial sector, sliding 10% each. FactSet Research Systems (FDS) shares fell 9% as Deutsche Bank cut its price target on the stock to $275 per share from $335.

Top decliners in industrials included Axon Enterprise (AXON), down 14%, and Equifax (EFX), down 11%.

Ulta Beauty (ULTA) was the worst performer in consumer discretionary, tumbling 17%. The beauty products retailer reported fiscal Q4 earnings per share below analysts' mean estimate and forecast fiscal 2026 EPS below Street views.

Just two sectors managed to post weekly gains: Energy climbed 2.1% while utilities eked out a 0.4% increase.

Occidental Petroleum (OXY) had the largest percentage increase in energy, rising 6.8%, followed by a 5.5% gain in APA (APA). Both stocks received price target increases from Barclays.

Next week, Dollar Tree (DLTR), Micron Technology (MU), FedEx (FDX) and Carnival (CCL) are among the companies releasing quarterly results.

The State of Private Credit & Bank Exposure

The Good, Bad and the Ugly

Private credit (or private debt) consists of debt-like, non publicly traded instruments provided by non-bank lenders -such as private credit funds and business development companies (BDCs)- to finance private businesses. These loans are typically privately negotiated, not issued or traded in public bond or loan markets, and are commonly extended to middle-market firms with annual revenue of roughly $10 million to $1 billion, though the market has expanded to include larger, historically leveraged-loan borrowers in recent years.

The US private credit market has expanded to over $1.7 trillion in assets under management as of mid-2023 — a roughly 10-fold increase since 2007. Some outlooks project AUM exceeding $2 trillion in 2026 and approaching $4 trillion by 2030. This is no longer a niche corner of the market — it's systemically significant.

The rapid ascent of the $1.7 trillion U.S. private credit market has sparked a polarized debate. Critics warn of a "shadow banking" bubble, while proponents see a resilient, necessary evolution of capital markets. To understand the health of our financial system today, we must look past the headlines at the structural interconnections between private lenders and traditional banks. For clarity, a shadow bank is a financial institution or vehicle that performs bank-like credit intermediations such as lending, maturity, and liquidity transformation—but operates outside the traditional, fully regulated banking system.

Some Legitimate Concerns

Back in October of last year Jamie Dimon commented on an earnings call regarding two high-profile bankruptcies, First Brands Group and Tricolor Holdings, both with large opaque private credit financing and some accusations of fraud. Dimon made the comment that when you see one cockroach, in this part of the credit market, there are probably more. JP Morgan Chase took a $170 million loss. This started the concerns about potential exposure to poorly run companies.

Since then, a wave of worry about climbing defaults on loans to software companies is setting up firms in the private credit market for a shakeout, according to Marc Rowan CEO of Apollo Global Management BlackRock (BLK) has meanwhile curbed withdrawals from its private credit fund after a surge in redemption requests, becoming the latest to be highlighted in the broader private credit issue. In addition, Blue Owl Capital permanently restricted withdrawals from its private credit fund and sold $1.4 billion in assets to a pension fund and to an insurance company whose assets it manages.

Deteriorating Borrower Health

So, here is what we know: the IMF's 2025 Financial Stability Report found that around 40% of private credit borrowers have negative free cash flow; this rate is up from 25% in 2021. That's a significant deterioration and the single most alarming datapoint in this debate.

The "True" Default Rate Is Being Obscured

While the headline default rates in private credit have remained below 2% for several years, once selective defaults and liability management exercises are considered, the "true" default rate is probably closer to 5%. Private credit companies are making concessions to their borrowers like allowing extension of agreements, accepting lower payments, so that they do not need to foreclose on a loan. The gap between the reported and true rates is a serious transparency problem and one of the biggest issues with the shadow banking system.

PIK Loans as a Stress Signal

Payment-in-kind (PIK) usage has risen notably, with public BDCs now receiving an average of 8% of investment income via PIK. Once limited to mezzanine and subordinated debt, PIK is increasingly appearing in senior secured loan documentation, a sign that borrowers are struggling to service debt with actual cash.

Bank Exposure Is Growing and Opaque

Bank loans to non-deposit financial institutions, which include private credit funds and related vehicles, reached roughly $1.14 trillion last year, according to Federal Reserve Bank of St. Louis data. A recent Whalen Global Advisors report warns of the growing exposure of US banks to private credit funds, credit managers, and private equity sponsors, noting conditions reminiscent of the 1920s when many believed asset values had reached a "permanently high plateau."

Valuation Integrity Under Scrutiny

The Department of Justice has publicly warned about "creative" marks and divergent valuation practices in private portfolios, while a high-profile SEC inquiry into Egan-Jones Ratings has placed the integrity of private credit ratings under the spotlight. Sage advisory The aborted Blue Owl fund merger also exposed fragility in semi-liquid structures when redemption pressure meets illiquid underlying assets.

Structural Contagion Risk

Private credit funds and traditional financial institutions are deepening ties, which could heighten contagion risk in a downturn. Here is what has been happening, the mechanism is pretty straightforward: Private Credit firms raise money from private investors, they then go to traditional banks and take loans to increase the amount they have to lend their borrowers and charge a premium since most lend to leveraged borrowers. This translates to exposure to the financial system because stress travels upstream quickly. Because the private credit space has gotten so competitive, the pressure to find opportunities is causing some lenders to do "dumb things" to boost income, mimicking behavior seen in the run-up to the 2008 financial crisis.

The Counterarguments

Why It May Not Be Systemic

Structural Buffers Exist

While headlines lead readers to feel like everyone who invested in BDC firms is struggling to get their money, most estimates indicate that roughly three-quarters of private credit capital comes from institutional investors (pensions, insurers, sovereign wealth funds (SWFs), and other funds), with the balance from retail/wealth channels and high-net-worth individuals.

Most of the current redemption pressure is coming from retail and wealth management investors in semi-liquid, non-traded private credit vehicles (especially perpetual BDCs and interval funds), rather than from large closed-end institutional drawdown funds. Since the time horizon is significantly different between individuals and institutions, an individual will typically have more short-term concerns than an institution. During the pandemic, some of the same Private credit firms invested in Las Vegas and other facilities impacted by the closure had the same challenge, with a handful of clients seeking to redeem their investments

Bank Stock Performance Doesn't Reflect Systemic Fear

For all the worries about private credit, the market doesn't appear to indicate major systemic trouble as we had in 2008. Banks, large and small, are outperforming both the Financials sector and global stocks over the past nine months despite recent private-credit casualties. Markets have seen the cockroaches and largely ignored them.

Recent Failures Appear Idiosyncratic

The collapse of a few companies, such as First Brand, Tricolor, and London-based Market Financial Solutions, involved fraud and "double-pledging" assets, using the same collateral for multiple loans. Fraud-driven failures, while alarming, are different from systemic underwriting failures.

Large Managers Are Bullish (With Caveats)

Ares Management argues that despite macro uncertainties, private credit portfolios continue to show resilience, with strong earnings growth, robust direct origination, and disciplined underwriting. Of course, these are interested parties — but their portfolios would be first to show cracks if the bears were right.

The Critical Unknowns

The honest answer is that opacity is the central problem. Unlike public credit markets, private credit has no mark-to-market pricing, no standardized disclosure, and valuation is often manager-determined. This creates three specific risks:

• Hidden losses that only surface when funds need liquidity

• Concentration risks that aren't visible until a sector-wide shock

• Systemic stress transmission through bank exposure to non-depository financial institutions (11.2% of bank loans) and insurance-PE partnerships

Conclusion

The difficult part of making an objective assessment in this segment of the financial industry is having access to the actual numbers. The media needs to create something to talk about, and many pundits who offer their opinion usually have some motive for their position. Some people have a glass that is half full perspective, and others have a glass that is half empty. While some firms have made dumb decisions, as Jamie Dimon had mentioned, not all of them have done so. Well-run firms have enough diversification throughout their entire portfolio that a handful of failed loans will not sink the firm. Companies like Apollo, Blackstone, and Ares can weather a handful of failures. The stock price of some of these companies is currently discounted significantly, and it may be an opportunity for a long-term gain if you have the capacity, tolerance for more volatility, and take the time to do some homework.

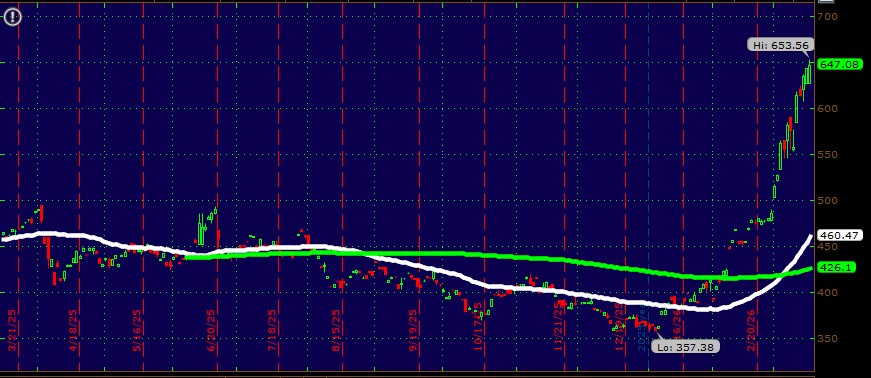

A Technical Perspective

The surge in oil prices has consumers concerned about gasoline costs, which were already rising ahead of the war in the Middle East. Looking at the chart of the S&P GSCI Unleaded Gasoline index (SPGSHU), gas prices rose steadily from the beginning of the year, then gapped higher in early February when initial signs of trouble arose around the Strait of Hormuz. The oil price shock didn’t appear until nearly a week after the strait was effectively closed, but gas moved well ahead of that date. The gasoline index is now up 75% from pre-war levels. Prices at the pump tend to lag oil by one to three weeks, and the national average may move closer to $4 per gallon if oil remains near $100 or spikes higher. Governments around the world are scrambling for solutions, including reductions or temporary elimination of fuel taxes, in addition to oil stockpile releases. As long as the Strait remains effectively closed, prices may continue their aggressive rise.