Newsletter

Week Ending February 20th 2026

In non-market-related news, on Sunday, February 22nd, the U.S. Olympic Hockey team won the Gold Medal against Canada in overtime. It had been 46 years to the day that the 1980 U.S Olympic Hockey team defeated the Soviet Union and went on to win the Gold Medal 2 days later against Finland. That event drove little kids into the sport of Ice Hockey and shifted the geographic footprint from just a niche sport primarily in the Northeast and northern Midwestern states (MN) to expand to southern states such as TX, FL, and the West Coast CA and NV. The NHL has grown by more than 50% since then and has become more popular, growing viewership by 30% annually. It is also worth noting that the U.S. women’s Hockey team also beat the Canadians for the gold medal, but the women teams has won gold twice since 2018 and 4 silver medals since 2002. Congratulations to both teams.

Market Recap

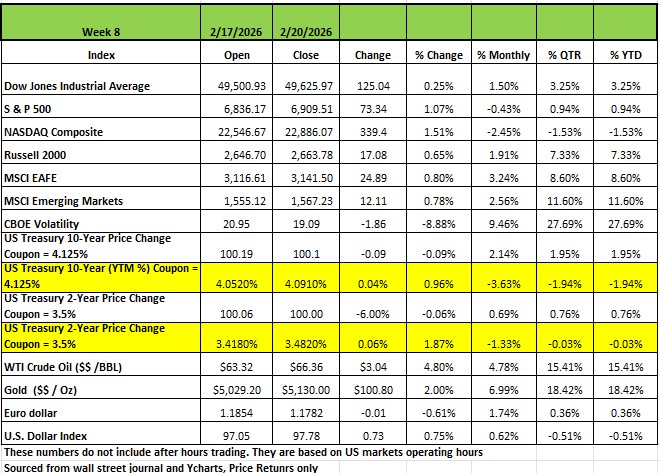

All four of the major indices finished the shorten trading week in positive territory for the week ending Feb 20th 2026, with the NASDAQ posting the largest increase of +1.51% on the week. The S&P 500 index rose +1.1% led by communication services, as investors digested changes to US tariff policy amid a Supreme Court ruling. The Russell 2000 finished up +0.65% and the DOW +0.25%. The S&P and the NASDAQ are both still down for the month of February

The drama in Washington continues as President Trump said on Friday he will sign an order imposing additional 10% global tariffs, under Section 122, after the Supreme Court invalidated his reciprocal tariffs imposed under the International Emergency Economic Powers Act.

"We are also initiating several Section 301 and other investigations to protect our country from unfair trading practices," Trump wrote in a social media post. The developments came as official data showed US economic growth was well below Wall Street's expectations in the final three months of 2025 as federal spending contracted due to the longest-ever government shutdown. Real gross domestic product rose at an annual rate of 1.4% in the December quarter, the slowest pace in three quarters; the consensus estimate was 2.8%, according to a Bloomberg survey.

A delayed release of economic data also showed US consumer spending growth unexpectedly held steady in December, while the Federal Reserve's preferred inflation metric accelerated more than Wall Street's estimates to 3% year over year.

Treasury yields rose slightly to moderately over the course of the week on speculation of rising geopolitical tensions and the Supreme Court striking down the tariff program. On Thursday, President Trump said that Iran will have to make a “meaningful deal” with the U.S. and implied that it will have to be within the next 10 days. Despite President Trump saying that both sides are engaged in “good talks” he did call Iran a “hot spot” right now and the Middle East has seen a vast buildup of military forces from the United States within the last few days. This led to a material rise in Oil prices, which ended the week up 6%.

By Sector

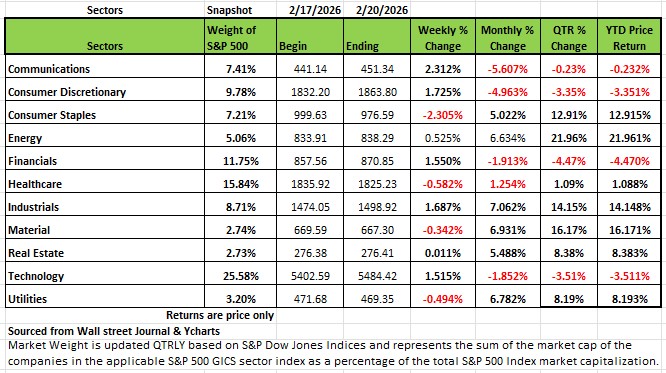

Seven of the 11 sectors were in the black last week. Communication services had the largest percentage increase of the week, climbing +2.3%, followed by gains of +1.7% each in consumer discretionary and industrials. Financials and technology added +1.5% each. Energy and real estate also eked out small gains.

Omnicom Group (OMC) led the gainers in communication services, jumping +21% as the company reported Q4 revenue above analysts' mean estimate and unveiled a $5 billion share-repurchase program, including $2.5 billion under an accelerated buyback. Omnicom also maintained its quarterly dividend rate.

Garmin (GRMN) shares led the climb in consumer discretionary as the company reported fiscal Q4 pro forma net income per share as well as net sales above analysts' expectations. Garmin also forecast 2026 pro forma earnings per share and revenue above Street views at the time. Shares rose +16%.

Deere (DE) was the top performer among industrials, climbing +9.9% as the company reported fiscal Q1 earnings per share and net sales above analysts' mean estimates. However, as of this writing, the stock is down $7.52 or -1.14% over concerns that farmers will be impacted by the new tariff rule.

On the downside, consumer staples fell -2.3%, followed by a -0.6% decline in health care and a -0.5% loss in utilities. Materials also edged lower. Walmart (WMT) was among the hardest-hit stocks in consumer staples, falling -8.1%. The retailer's fiscal Q4 adjusted earnings per share and revenue slightly surpassed analysts' mean estimates, but its guidance ranges for fiscal Q1 and fiscal 2027 adjusted EPS came in below Street views.

This week's earnings calendar features Home Depot (HD), Constellation Energy (CEG), NVIDIA (NVDA), TJX (TJX), Salesforce (CRM), Lowe's (LOW) and Berkshire Hathaway (BRK.A, BRK.B). Economic data will include February consumer confidence and a delayed report on the January producer price index.

The Great Rotation Continues?

For the better part of a decade, the investment thesis was straightforward: the United States was the only game in town. While Europe flirted with recession and China grappled with a property crisis, the American consumer remained a relentless engine of global growth. Resilient consumers, a tight labor market, and an AI-fueled earnings boom kept domestic equities leading every global league table. Investors who chased diversification abroad were largely punished for their effort. That playbook may now be getting a rewrite — and the PMI data is one of the clearest signals yet

Friday’s Flash PMI data revealed a "Great Divergence" that should catch the eye of every macro investor and business owner. While business activity in Japan and the UK is hitting multi-year highs, the U.S. just slipped to its lowest level in nearly a year. Source (https://www.spglobal.com)

The Numbers: A Tale of Two Tapes

The preliminary S&P Global Composite PMI figures for February highlight a widening gap between the U.S. and its developed-market peers:

United States: The Composite PMI fell to 52.3 (a 10-month low), down from 53.0 in January. Both manufacturing and services cooled, with factory orders declining and employment growth effectively stalling at 50.2.

United Kingdom: In a stark contrast, the UK climbed to a 22-month high, signaling that the British economy is finally catching its second wind after a sluggish 2025.

Japan: Leading the pack, Japan’s expansion hit a 33-month high (PMI at 52.8). Driven by robust export demand and the "AI semiconductor" boom, Japanese manufacturing is growing at its fastest clip in nearly four years.

What is driving the U.S. Slowdown?

The culprits are not hard to identify. Tariff uncertainty is front and center. Survey respondents have repeatedly cited import costs as a driver of both elevated prices and softening demand, a toxic combination that squeezes margins while limiting top-line growth. New export orders have declined for seven consecutive months, reflecting deteriorating competitiveness and retaliatory measures from trading partners. Despite the Supreme Court’s recent ruling against broad executive use of the IEEPA for tariffs, the "Pivot to 122" (the new 15% surcharge) and ongoing trade uncertainty are weighing heavily on manufacturing. Export demand for U.S. goods saw one of its sharpest declines in the past year, as international buyers increasingly seek non-U.S. alternatives

The manufacturing sector has been particularly exposed. Over the past three months, factories have consistently produced more goods than they've sold, an inventory accumulation dynamic that S&P Global notes "hasn't been seen to this degree since the global financial crisis of 2009". This excess stock either gets discounted or production gets cut, neither of which bodes particularly well for near-term earnings or employment in the sector.

Spending Aversion & Affordability: After years of high prices, the American consumer is showing signs of fatigue. S&P Global economists noted that "spending aversion" is now evident in the data, as households and businesses push back against persistent input cost inflation

Why the Rest of the World Is Gaining Ground

The improvement abroad isn't coincidental; it's structural. Europe's uptick is being driven in large part by fiscal stimulus, with increased defense spending creating a meaningful demand tailwind across German and broader continental manufacturers. The European Central Bank's rate-cutting cycle has also begun working its way through the economy, easing credit conditions. UK consumers and service businesses appear to be benefiting from a combination of falling energy costs and improving confidence following the government's budget passage.

Japan's situation is different but arguably more durable. The country's business activity hit a 33-month high on the back of strong export demand, particularly in advanced manufacturing and semiconductors tied to the global AI infrastructure buildout. Taiwan and South Korea are benefiting from the same dynamic, with their PMI data showing multi-month highs powered by chip and component demand. Emerging markets broadly posted an +8.9% total return in January, led by gains in Korea and Taiwan.

There is also a counterintuitive element at play: U.S. tariff policy, designed to protect domestic manufacturers, is paradoxically opening new export opportunities for other countries. S&P Global's survey data shows companies in China, Canada, and across Southeast Asia actively reporting new trading relationships as global supply chains re-route away from U.S. markets.

This divergence represents more than just data print; it's a symptom of institutional friction. The U.S. is currently navigating a period of intense internal legal and political maneuvering, from government shutdowns to SCOTUS battles over executive power.

While the U.S. is bogged down in "Crisis" era restructuring, other economies (notably Japan) are capitalizing on the global technology race. We are seeing a "Great Rotation" where capital is beginning to flow toward markets that offer more policy stability and lower valuations compared to the crowded U.S. tech trade.

The U.S. isn't out of the race, but the "exceptionalism" premium –(the extra multiple that investors have been willing to pay for U.S. stocks precisely because American growth, earnings, and innovation were seen as reliably superior to anything available elsewhere) is being tested That premium is reflected in the S&P 500 trading at roughly 28x earnings versus 18x for domestic small caps and even lower multiples for most international developed markets

Keep a close eye on these three releases to see if the slowdown is a temporary blip or a trend:

Consumer Confidence (Tuesday): Will it confirm the "spending aversion" seen in the PMI?

NVIDIA Earnings (Wednesday): Can the AI goliath single-handedly lift U.S. sentiment?

U.S. PPI (Friday): If wholesale inflation remains hot despite slowing activity, the "Stagflation" word will start appearing in headlines again.

The "U.S. vs. The World" trade is no longer a one-way street. For the first time in this cycle, the UK and Japan are not just participating; they are leading. It would be premature to write off American exceptionalism entirely. In market terms, the phrase refers to the sustained tendency of the U.S. economy and by extension U.S. equities to outgrow and outperform the rest of the developed world, driven by superior productivity, deeper capital markets, stronger corporate earnings growth, and a more flexible labor market. It's the thesis that justified years of home-country bias and punished investors who diversified away from U.S. assets

What the PMI data does confirm is that the gap between the U.S. and the rest of the world that made the home-country bias so profitable over the last two years is narrowing. Whether it continues to close or snaps back is the key question for global allocation in 2026. The data bears watching closely.

The Week Ahead

The economic calendar is light this week, leaving investors with more time to ponder the potential consequences of the U.S. Supreme Court’s momentous decision on tariffs. The big question will be whether the government must refund tariff revenue, how much might have to be paid back, and over what timeframe. The administration’s response to the ruling is a source of uncertainty, along with how the U.S. would replace the expected future revenue that could have been used to service its debt. Bond prices may come under pressure as worries resurface over government finances, which could push longer-term yields higher. The decision could also affect sectors that derive significant revenue from non-U.S. sales, as well as those sensitive to raw material and component prices. One of the most important earnings announcements of the season arrives on Wednesday after market close. Nvidia is expected to report earnings and revenue growth around 70% YoY, but investors are likely to zero in on gross margins and forward guidance. Retailer Home Depot also reports this week. On the economic calendar, Friday’s Producer Price Index will be the main release of interest, as a hot reading could weigh on rate cut expectations. Consumer confidence and factory orders are also on the docket. There are many appearances from FOMC members this week with opportunities to comment on recent developments. On the international side, inflation updates in Germany, Japan, and Australia are the releases of note