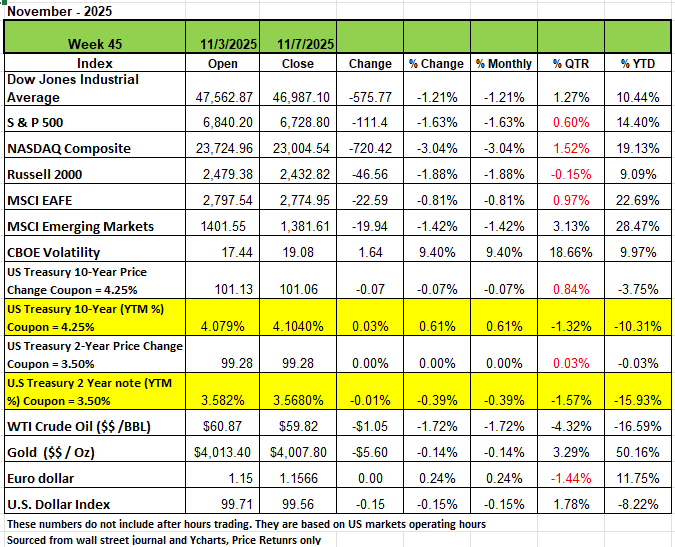

All four of the major indices ended the first week of November down significantly with the NASDAQ seeing the steepest de4cline of -3.04% followed by Russell 2000 -1.88% the S&P posted a -1.63% and the DOW had a return of -1.21%. The shutdown has led to concerns of economic data and the health of the economy with little information coming from 3rd parties such as ADP and Challenger Gray and Christmas who released a report on Thursday Nov 6th that U.S.-based employers announced 153,074 job cuts in October, up 175% from the 55,597 cuts a year earlier in October 2024. It is up 183% from the 54,064 job cuts announced one-month prior Economic readings have been sparse for the past month as the government shutdown has delayed multiple reports. Treasury yields finished the week mixed, with shorter-duration yields mostly lower while longer-duration yields ticked higher. Last Wednesday, the government shutdown entered its 36th full day, officially making it the longest shutdown in U.S. history. Earlier in the week investors received a rare update on the economy amid the economic data blackout. The ISM Manufacturing Index declined to 48.7 in October, falling short of the consensus expected 49.5. This is the eighth consecutive month that the index has been below 50 (signaling contraction) as the manufacturing sector continues to struggle for traction. Meanwhile, demand remains subdued as just four of the major manufacturing industries reported growth in new orders. On the other hand, the ISM Non-Manufacturing Index increased to 52.4 in October, beating the consensus expected 50.8. The service sector, responsible for two-thirds of U.S. output, remains far more resilient with activity expanding in ten out of the last twelve months. On Friday, the University of Michigan Consumer Sentiment Index posted a reading of 50.3 for November, falling short of the consensus expected 53.0. This marked the lowest reading in more than three years as consumers are growing increasingly concerned about the broader economic effects of the prolonged government shutdown.

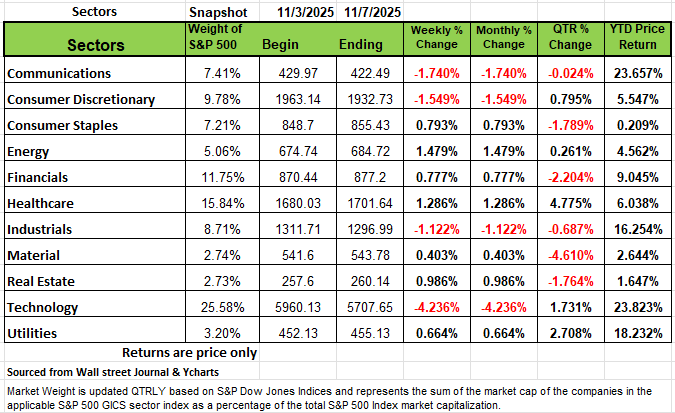

By Sector

On the sector side Four of the 11 sectors that make up the S&P 500 were in the red with Technology posting a -4.23% decline, followed by Communications -1.74% Consumer Discretionary -1.54% and Industrials -1.12%. Super Micro Computer (SMCI) had the largest percentage drop in the technology sector, with its shares falling -23%. The company reported fiscal Q1 adjusted earnings and revenue below analysts' mean estimates and forecast fiscal Q2 adjusted earnings per share below the Street view, even as the company raised its fiscal 2026 net sales guidance. In communication services, shares of Take-Two Interactive Software (TTWO) fell -9.5% as the company reported a wider-than-expected fiscal Q2 loss and delayed the launch of its Grand Theft Auto VI game. Still, a number of sectors rose this week. Energy advanced +1.5%, followed by a +1.3% rise in health care and a +1% increase in real estate. Consumer staples, financials, utilities and materials also edged higher. The gainers in energy included Targa Resources (TRGP), which reported Q3 net income up from the year-earlier period and above analysts' mean estimate. The company also priced a public offering of $750 million of 4.35% senior notes due 2029 and $1 billion of 5.4% senior notes due 2036. The offerings were priced at 99.938% and 99.92% of the notes' face value, respectively. Shares rose 12%. Earnings reports this week are expected from companies including Cisco Systems (CSCO), Walt Disney (DIS) and Applied Materials (AMAT).

The Senate Fight over Healthcare subsidies

As of the writing of this article, the government shutdown looks like it is finally coming to an end with several members of one party breaking ranks and voting to end the shutdown. The key issue behind the current the shutdown is a deeply entrenched dispute between Republicans and Democrats over healthcare funding provisions, particularly the extension of premium tax credits that subsidize health insurance and the reversal of recent Medicaid cuts. Republicans and Democrats have both proposed funding bills, but each party’s proposal was rejected by the other in the Senate, primarily due to disagreements over healthcare subsidies for the Affordable Care Act (ACA) and broader control over appropriated government spending. So, we thought perhaps we would explore and take an unbiased look at the healthcare landscape and see why it is not working.

First, we want to remind our readers that the U.S. government is in debt. Currently, the debt obligation is over $36 trillion dollars, and we run an annual deficit of just under $2 trillion dollars. To put this in perspective, it is about $112,000 per individual in the U.S and $288,000 per household. So keep this in mind when you think about the issues in Washington D.C.

When the Affordable Care Act was signed into law in 2010 and fully implemented in 2014, it came with bold promises: expanded coverage, controlled costs, and a reformed healthcare system that would work for all Americans. Now, a decade later, the evidence tells us a different story. While the ACA succeeded in expanding insurance coverage to millions of Americans, (mostly those with pre-existing coverage and to those who could not afford the insurance premiums) it has failed spectacularly at its primary goal—making healthcare affordable. The fundamental problem? The ACA attempted to fix healthcare by focusing on one segment and controlling the insurance layer while ignoring the deeper structural issues plaguing America's healthcare system.

Healthcare in America is too fragmented to control. For example, just look at drugs: We have Pharmacies, pharmaceutical manufacturers, pharmaceutical distributors, and Pharmacy Benefit Management (PBM). There are outpatient medical facilities, hospitals, manufacturers for MRI’s X-rays, and surgical robotic equipment, with wholesalers and distributors, as well as warehousing and logistics companies for those companies. Some companies specialize in making Hospital beds to band aids and the distribution chain for those products. We have universities that train and educate Doctors and other healthcare workers. Physicians spend hundreds of thousands of dollars on their education before being able to generate any income. Then there are insurance companies on multiple levels, insurance to protect the facility from malpractice, the workers' compensation insurance, the property insurance and then lastly the health insurance companies that pay the bills for the service provided. Health insurance is also a bit confusing with language most Americans are unaware of definitions such as deductible, coinsurance, and most importantly, the network, care providers participate in.

In evaluating the law behind the ACA, we find a few issues extremely challenging. The first issue is that every legal resident in the U.S. was required to buy insurance, and if they fell below a certain income level, they either received a premium subsidy with one of the major carriers or they would qualify for Medicaid. These payments were funded by tax dollars. If you did not enroll in a qualified ACA plan, you were taxed at year's end. From 2016 through 2018, the penalty was the greater, of $695 per adult (and $347.50 per child, up to a maximum of $2,085 per family). Insurance premiums were significantly higher than the penalty so for a family that did not qualify for a subsidy and did not want to pay for health insurance, the tax penalty was a lot cheaper. In looking at the math, the IRS collected about $3 billion in tax penalties on approximately 6.5 million taxpayers in 2015. However, the government paid over $18 billion in subsidies alone in 2014 and over $495 billion in Medicaid, a 60% increase from before the law was passed.

The official document/law for the ACA is over 906 pages; however, when all the implementing rules and regulations are included, the page count is estimated to be around 11,000 pages long. One well-known politician even said, “We have to pass the bill so that you can find out what is in it". This may be one of the biggest problems with our government and why anytime the government gets involved in something, it screws it up most of the time. When the government gets out of its lane, it has historically messed up everything it touches, including both sides of the aisle. Perhaps the one detail about the Affordable Care Act that has contributed to skyrocketing health premiums is the rule that Health insurance carriers need to use 85 % of premiums collected on claims, and if not used, then refunds are issued to policyholders. This means that insurance carriers must operate on a 15% margin. In that margin are broker commissions, administrative and marketing costs.

This is what we feel is a big issue to the rising cost, because insurance works off of a pool. You cannot drain a pool for one year and then expect the following year not to refill it. This is done with higher premiums. Remember, all companies associated with the healthcare industry are in business to make money; if they don’t make money, then they go out of business, and we are left with fewer choices. Since the ACA was passed a number of companies have left the market. In Illinois, we have seen UniCare, Celtic, American Medical Security, and Humana leave the marketplace. Humana is now in the health supplement business with a focus on Medicare. The others have either gone out of business or have been purchased. In the State of Illinois, there are basically 2 insurance carriers Blue Cross Blue Shield of IL and United Healthcare. In the group marketplace, we can add Aetna, but that company no longer serves the individual market. In the New York Metropolitan area, Aetna withdrew from the group marketplace

The cost of health insurance has risen so much faster than any other industry. Since the ACA was passed, we have seen a lot of mergers of Health providers and a battle between insurance carriers and medical facilities over claims reimbursement rates. Between 2000 and 2020, there were over 1,600 hospital mergers involving thousands of facilities. This unprecedented wave of consolidation has fundamentally altered the competitive landscape of American healthcare. By 2017, in most markets, a single hospital system controlled more than 50% of market share. The median hospital market concentration (measured by the Herfindahl-Hirschman Index) increased from 2,163 in 2010 to 5,078 in 2022—a dramatic shift toward monopolistic market structures.

The evidence on consolidation's impact is unequivocal: mergers lead to higher prices without corresponding improvements in quality. Studies show that: Hospital mergers increase prices by an average of 1.6% to 5.2% overall Mergers creating significant market power can raise prices by 20% to 50% Cross-market mergers (hospitals in different geographic areas) raise prices by 10% to 17% When hospitals acquire physician practices, prices for the same services increase by 14% on average

Research by leading health economists has found that "hospitals that have fewer potential competitors nearby have substantially higher prices." A hospital without competitors within a 15-mile radius charges prices 12% higher than hospitals in markets with four or more competitors. This market power allows hospitals to extract higher payments from insurers, who then pass these costs on to employers and consumers through higher premiums. The increase in premiums has also led to a surge of non-compliant health plans that pay a very limited dollar on claims. These types of health care plans mislead people into believing that they are covered in case of an emergency. They require underwriting, so they try to keep their pool healthy and play the odds that they will have claims limited to minor issues. However, when a person gets hospitalized, they usually get hit with large medical bills, which all patients are responsible for at all times.

Many other factors contribute to the rising cost of healthcare, and we are not going to list all of them. But perhaps the single biggest contributor to America’s healthcare problem is that, as a society, we have a very unhealthy lifestyle; we eat more processed foods, especially on the run. We don’t exercise and put ourselves in stressful situations because we don’t prioritize our finances. We overspend, undersave, and overleverage ourselves because we need bigger homes, newer cars, and other gadgets. We address our wants before our needs and expect to be bailed out when we make poor decisions. This added stress leads to a lot of health issues, especially cardiac issues and depression.

This article is provided by Gene Witt of Optimized Capital LLC. for general informational purposes only. This information is not considered to be an offer to buy or sell any securities or investments or to be considered investment advice. Investing involves the risk of loss and investors should be prepared to bear potential losses. Investments should only be made after thorough review with your investment advisor, considering all factors including personal goals, needs and risk tolerance. Optimized Capital Registered Investment Adviser (RIA) that maintains a principal place of business in the State of Illinois and Indiana. The Firm may only transact business in those states in which it is notice filed or qualifies for a corresponding exemption from such requirements