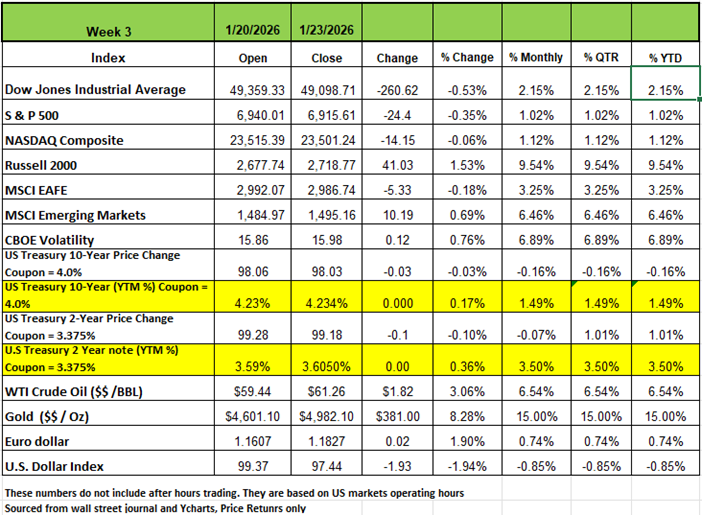

Last week was a short and volatile week, with markets closed on Monday Jan 19th for MLK birthday holiday. It was also the week of the WEF (World Economic Forum) held in Davos where political and business elites discuss global, regional, and industry agendas. The week started off on a decline as markets were concerned about Greenland becoming part of the U.S. the S&P (-2.06%) & NASDAQ (-2.39%) both down by more than -2% and the DOW dropping (-1.76%) and the Russell 2000 (-1.21%). However, on Wednesday the President announced that the US would not take military action and that a deal was made. Markets responded positively Gold took a large bump of $381/oz and at the time of this writing the price has surpassed the $5000 mark up another +2.1% on the day Last week Newmont mining rose +8.96%. The DXY (dollar index) dropped by -1.94% and Crude oil WTI rose 3.06% to $61.26 /barrel Quarterly earnings reports were mixed this week. Earnings from financial companies including Capital One Financial (COF) and Charles Schwab (SCHW) missed expectations, weighing on the market. Worries about the technology sector also increased as chip maker Intel (INTC) issued a weaker-than-expected forecast for the current quarter despite posting higher-than-expected Q4 results.

Treasury yields rose sharply early in the week amid all of the geopolitical tensions and tariff threats but later declined as those concerns eased, leaving yields relatively unchanged by week’s end. US mortgage applications for home purchases jumped 14.1% last week, reaching their highest level since January 2023. The surge was driven by lower borrowing costs, with mortgage rates falling to their lowest point since September 2024. The economy posted strong headline growth in Q3, with real GDP revised up to a 4.4% annual rate, the fastest in two years. The increase reflected gains in inventories, business investment (primarily structures), and net exports, which helped offset softer homebuilding and consumer services. Core GDP rose at a 2.9% annual rate, consistent with its long‑term pre‑COVID trend. Overall real GDP is up 2.3% from a year earlier, slightly below but near its pre‑pandemic peak of 2.4%. Personal income rose 0.3% in November, coming in slightly below the consensus forecast of a 0.4% increase. Personal consumption climbed 0.5%, in line with expectations. Over the past year, personal income has grown 4.3%, while consumer spending has risen 5.4%. Growth was driven largely by private‑sector wages and salaries, which increased 0.4% in November after a 0.5% gain in October. One of the big focal points this week will be the funding of the budget, which was extended back in November after the longest close in US government history.

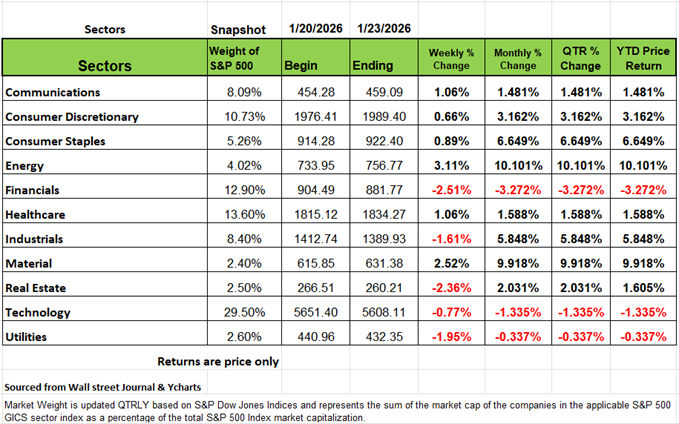

By Sector

The energy and materials sectors climbed, helping to minimize the S&P 500's overall drop, as companies including oilfield services company SLB (SLB) and metals company Freeport-McMoRan (FCX) still surpassed analysts' mean estimates. The Financial sector had the largest percentage decline this week, falling -2.5%, followed by a -2.4% loss in real estate and a 2% drop in utilities. Industrials and technology also moved lower. Capital One Financial was among the financial sector's hardest-hit stocks, sliding -9.1%. The company's Q4 adjusted earnings per share missed analysts' mean estimates despite a slight revenue beat. The company also said it agreed to buy AI-powered financial software platform Brex for $5.15 billion in cash and stock. In addition Blackstone (BX) was down -7.98% and KKR decline -7.75% and Ares Capital (ARES) -8.11% Interactive Brokers (IBKR)was up +5.77%

Weighing on the Technology sector, shares of Intel fell -4% as the company flagged supply disruptions. The company also said during its Q4 earnings call that it now expects higher 2026 capital expenditure compared with its initial guidance.

On the upside, the Energy sector rose +3.1%, with EQT posting a 9.84% gain Expand Energy (EXE) +9.67% Devon (DVN and Coterra Energy (CTRA) both up +6.7%. SLB was among the energy sector's top performers, climbing to +5.2%. The better-than-expected Q4 results from the company, formerly known as Schlumberger, were driven by double-digit revenue growth in its digital and production systems divisions, as well as stabilizing global upstream activity

There was a +2.6% advance in Materials with Albemarle Corp (ALB) + 16.17% and the Mosaic Co (MOS) +9.26% Freeport-McMoRan rose +2.9%, boosting the sector. In Communication services rose +1.1% with META up +6.17% and Comcast (CMCSA) +5.39%. Netflix declined -2.15%. In Healthcare. Moderna (MRNA) popped +16.11% and Abbott Labs (ABT) dropped -11.79%. Consumer Staples and Consumer Discretionary also edged higher. This week's earnings calendar features a number of large companies including UnitedHealth Group (UNH), Microsoft (MSFT), Meta Platforms (META), Tesla (TSLA), International Business Machines (IBM), AT&T (T), Apple (AAPL), Visa (V), Mastercard (MA), Caterpillar (CAT), Exxon Mobil (XOM), Chevron (CVX), American Express (AXP) and Verizon Communications (VZ)

The Gold Barometer: Fragile Powers and the New Geopolitical Hedge

The surge in gold prices over the past year (spot gold) has risen roughly 64% in 2025 and so far this year its risen another 15–17%, recently breaking above $5,000 per ounce, and according to many forecasts, headed toward $5,500–$6,000. Gold is tightly correlated with the very geopolitical tensions. China’s internal power struggles, Russia’s grinding war losses, Iran, Venezuela and perhaps the U.S.’s more coercive, “bullying” style of diplomacy. In effect, gold is behaving as the default hedge against three overlapping risks: great power confrontation, institutional fragility, and a weakening faith in the dollar-centric financial order. As political systems strain and great power frictions intensify, investors and central banks are quietly expressing a common judgment: they trust hard assets more than they trust any of the major players. Three stressed powers, one uneasy world In Beijing, Xi Jinping’s sweeping purge of top generals signals both ambition and anxiety. He has removed or sidelined much of the senior military leadership he previously elevated, hollowing out the top of the chain of command in the name of anti-corruption and loyalty. The result is a People’s Liberation Army (PLA) that may be more politically obedient, but also more brittle. Creating an institution where career survival depends on personal fealty rather than professional judgment at a time when Taiwan, the South China Sea, and U.S.–China rivalry all raise the odds of miscalculation. In Moscow, the Kremlin is waging a war of attrition that treats Russian soldiers as expendable inputs. Years into the invasion of Ukraine, casualty estimates suggest a staggering loss of life, with waves of mobilized men and volunteers thrown into what even Russian sources have described as a “meat grinder.” It is estimated that since 2022, some 250,000 soldiers have been killed. If you include the wounded the numbers exceed 1 million casualties. The cost is a significant change to the country’s demographic makeup —lost sons, fathers, and workers in an already aging society the highest number of casualties are men between the ages of 35-40. Estimates suggest that between 500,000 and over 1,000,000 Russian citizens have already left the country since 2024, driven by fears of conscription, mobilization, and political repression. This drain on the Russian population will echo through the country’s society and economy for decades, even if the government can temporarily suppress public anger and dissent.

In Washington, U.S. power still rests on unmatched military reach and control over the global financial infrastructure, but what is different now is the way in which it is exercised. Sanctions, secondary sanctions, tariff threats, and public brow-beating of allies have become routine tools of statecraft. What critics call a “bullying” style of diplomacy may win short term concessions, yet it also accelerates efforts abroad to hedge against American leverage—from new regional blocs and alternative payment systems to a quiet rethink of how much exposure governments want to the dollar itself. China’s military purges, Russia’s mounting casualties, and America’s coercive diplomacy are not isolated phenomena; they are interconnected responses to a more contested, multipolar world. Xi’s consolidation of personal control over the PLA reflects both ambition and insecurity about the reliability of the forces that would be central in a confrontation with the U.S. and its allies, particularly over Taiwan Russia’s willingness to burn through hundreds of thousands of lives to sustain its war in Ukraine reflects a regime that sees battlefield defeat as existential, even at the cost of long term demographic and economic decline. U.S. “bully diplomacy,” in turn, reflects a superpower still capable of imposing significant pain through sanctions and market access, yet increasingly frustrated that traditional tools no longer guarantee compliance in a world where China and Russia offer alternative partnerships, even if those alternatives are costly or fragile. The world is entering a phase where the leading powers are simultaneously more brittle at home and more willing to project pressure abroad, raising the stakes of every crisis from the Taiwan Strait to the Donbas and the Persian Gulf Each power is responding to internal weakness as much as external rivalry: China by tightening personal control over its armed forces, Russia by sacrificing a generation to preserve regime survival, and the U.S. by leaning harder on its financial and military dominance even as its relative standing slowly erodes. The mix of centralization, desperation, and overreach raises the risk that the next crisis will escalate further and faster than markets have grown used to.

The Gold Play

Gold has become the real-time barometer of global unease. In the last 12 months, gold has surged to record highs, blasting through the psychological barrier of $5,000 an ounce as of today and doing so without the kind of systemic banking panic that typically explains such moves. Interest rates matter, as do expectations that central banks will eventually ease, but the scale and speed of the rally tell you something else: markets are pricing in a geopolitical risk regime. At the moment, this seems like a commonsense trade with China’s internal purges and unresolved flashpoints with the U.S. having elevated tail risks in Asia. Russia’s willingness to absorb extraordinary casualties in Ukraine shows that the war is not “manageable background noise,” but an open wound that can still infect energy, food, and cyber domains. America’s heavy use of financial and trade coercion warns other states that dollar assets could be turned into pressure points overnight. In that world, gold’s attraction seems obvious: it carries no promise that can be broken by a foreign government, no payment system that can be switched off, no boardroom that can be sanctioned. Perhaps this is why central banks, especially in emerging markets and among U.S. rivals and wary partners, have been some of the most consistent buyers. For them, gold is not a speculative trade; it is a strategic asset, a form of insurance against being on the wrong side of the next sanctions package or the next great power rupture. For private investors, the message is similar: if the institutions and alliances that underpinned the last 30 years of globalization are fraying, then a larger allocation to assets outside that system looks less like fear and more like prudence. For several generations, markets learned to look through geopolitical noise on the assumption that institutions were strong, leaders were predictable, and any conflict would be quickly contained. Today’s environment looks different. We see a Chinese leadership that trusts its generals less, a Russian regime willing to burn through its own future, for ego and an American foreign policy that increasingly weaponizes its financial dominance all point to a more volatile, less rule-bound world. Gold’s meteoric climb seems to be the market’s way of saying that this isn’t just talk. It is the price signal that ties these stories together, a reflection of deteriorating trust in political judgment, institutional checks, and the durability of the existing monetary order. You can disagree on which country bears the most blame, or on whether gold is overbought in the short term. But as long as the three big powers are governed more by fear and force than by restraint and confidence, the case for some form of “geopolitical insurance” in portfolios will remain very much alive, and gold will stay at the center of that conversation.

The Week Ahead

The shifting geopolitical landscape’s effect on sentiment was evident last week, reviving talk of the “Sell America” trade that emerged after last April’s sweeping tariffs announcement. Investors await more details on negotiations between the U.S. and NATO regarding Greenland while also looking to corporate earnings and the Federal Reserve meeting. The Fed is widely expected to keep rates steady when it announces its policy decision on Wednesday, but questions around the central bank’s independence may be more top-of-mind for this meeting. The busiest week of this corporate earnings season provides investors with an opportunity to see how artificial intelligence-related investment is progressing. Quarterly updates from Apple, Meta Platforms, Microsoft, Tesla, UPS, Boeing, Chevron, and many more are on the docket. The U.S. economic calendar includes consumer confidence, durable goods and factory orders, and the producer price index. The Bank of Canada is also expected to keep rates unchanged this week, as the country’s economy is holding up reasonably well in the face of U.S. tariffs. In Europe, the first estimate of Q4 GDP arrives on Friday along with Germany’s December CPI. Inflation updates from Japan and Australia are also on the international calendar. Odds are rising that the Bank of Australia may raise rates at its meeting next month, with inflation on the rise, while an extension of recent declines in Japan’s CPI may put additional pressure on the yen.