The Art of the Pivot: Decoding the Shifting Interest Rate Outlook

This article is provided by Gene Witt of Optimized Capital LLC. for general informational purposes only. It is an opinion, not investment advice. This information is not considered to be an offer to buy or sell any securities or investments, and again not to be considered investment advice. Investing involves the risk of loss, and investors should be prepared to bear potential losses. Investments should only be made after a thorough review with your investment advisor, considering all factors, including personal goals, needs, and risk tolerance. Optimized Capital Registered Investment Adviser (RIA) that maintains a principal place of business in the State of Illinois and Indiana. The Firm may only transact business in those states in which it is notice filed or qualifies for a corresponding exemption from such requirements.

Market Recap November 25th 2025

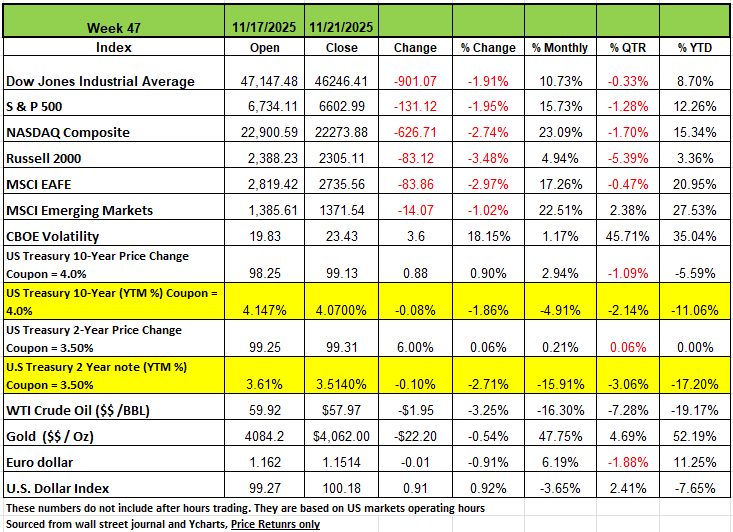

All four of the major indices posted negative returns for the week ending Friday, November 21st, with the Russell 2000 posting the largest decline -3.48% followed by the NASDAQ -2.74%, the S&P500 -1.95% and the DOW -1.91%. Financial markets were particularly volatile last week, still torn between the high valuations of US tech giants, despite Nvidia's better-than-expected results. Unemployment statistics, published late due to the government shutdown, confirmed the strength of the US labor market, further delaying the prospect of a Fed rate cut in December. Volatility has increased significantly, and this nervousness is likely to continue throughout the rest of the year.

The market benchmark ended Friday's session at 6,602.99. It is now down -3.5% for November but up +12% for the year.

September payrolls in the US rose by +119,000, more than the 51,000 increase expected in a Bloomberg survey. The unemployment rate edged up to 4.4%, the highest since October 2021, while Wall Street had expected it to hold steady at 4.3%.

The report was delayed by almost seven weeks by the record-long federal government shutdown, which ended last week.

Investors are weighing what the data might mean for the Federal Reserve's December policy meeting. Minutes from the October meeting showed policymakers held "strongly differing views" on the next rate decision.

The Labor Department will not publish the October jobs report; instead, including those payroll figures in the November report due out December 16, which is after the Fed’s December meeting. The minutes from the Fed’s October meeting, released last week, showed mixed views regarding a rate cut at its December meeting, creating uncertainty over the Fed’s next move. The market-implied probability of a rate cut at the Fed’s December meeting dropped to roughly 30% on the news, down from 46% the day prior and 68% at the end of last month. However, the President of the New York Fed said Friday he sees room for a rate cut in the near term, saying upside risks to inflation have eased while downside risks to employment have increased. The comments significantly increased the market’s expectations for a December rate cut, capping a volatile week. Consumer sentiment fell in November to near record lows, according to the University of Michigan’s Consumer Sentiment Index. High prices and weakening incomes weighed on sentiment.

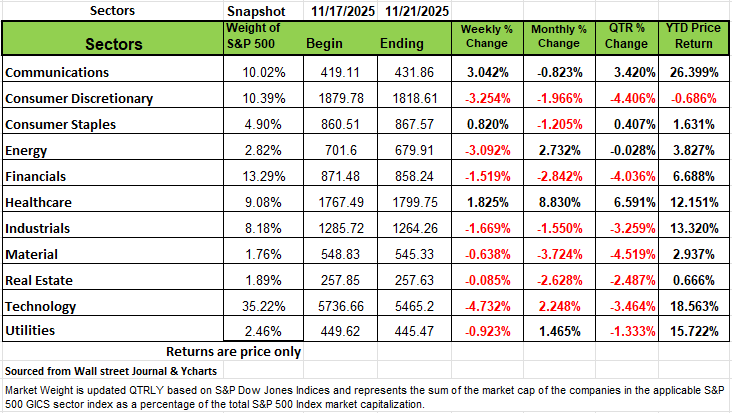

Sectors

On the upside, the Communications sector was up +3.04% followed by Healthcare sector +1.8% and consumer staples 0.82% The rest of the sectors all posted negative returns on the week. Technology led the sectors decline this week, falling -4.7%, followed by a -3.3% slide in consumer discretionary and a -3.1% drop in energy. Industrials, financials, utilities, materials and real estate also fell. Advanced Micro Devices (AMD) shares fell 17%, and Micron Technology (MU) dropped 16%. Nvidia shed 5.9% despite stronger-than-expected fiscal Q3 results.

Wedbush described the selloff as another "DeepSeek Moment," noting investor nerves around the sustainability of the AI buildout. Among the top decliners in consumer discretionary, Home Depot (HD) shares fell -5.25% this week. The home-improvement retailer's fiscal Q3 earnings unexpectedly fell, and the company lowered its bottom-line outlook for the full year.

The energy sector's drop came as crude oil futures also fell on the week. EQT Corp. (EQT) shed 4.8% and Marathon Petroleum (MPC) declined -4.7%. Communication services climbed 3%, health care rose 1.8%, and consumer staples edged up 0.8%. Alphabet's (GOOGL, GOOG) shares rose 8.4% as its Google unit unveiled Gemini 3, its latest artificial intelligence model. Next week, the market will be closed on Thursday for the Thanksgiving holiday, followed by a shortened session on Friday, known as "Black Friday."

Earlier in the week, economic data will include September retail sales and the September producer price index. Both reports were delayed by the government shutdown.

The Art of the Pivot:

Decoding the Shifting Interest Rate Outlook

The path of interest rates is arguably the single most important variable in global markets today. For months, central banks worldwide have been executing the fastest monetary tightening cycle in decades to combat surging inflation. The spike in Inflation was a result of the deployment of trillions of dollars during the pandemic to help those that were not able to work or had reduced hours. Now, that inflation is showing signs of moderating and economic growth is slowing, the focus has now shifted from "How high will rates go?" to "When will they start to fall again?"

This transition from a hiking cycle to a potential easing (cutting) cycle is referred to as the "pivot," and the shifting outlook around its timing and magnitude is what is causing significant volatility across asset classes. Many believe that rates should go back to pre-pandemic levels, especially home buyers, since the real estate market is impacted by rates.

The Central Bank's Tug-of-War: Data Dependence

Central banks, such as the U.S. Federal Reserve (Fed), operate with a dual mandate: They need to achieve maximum sustainable employment and price stability (managing inflation) currently the target is still 2% but the annual inflation rate is at 3%. Interest rate decisions are not pre-set but are highly data dependent.

The debate among policymakers’ centers on which of the primary economic signals poses the greater risk:

The Inflation Risk (The "Hawks"):

This group of Policymakers worried about inflation remaining stubbornly high may advocate keeping interest rates at restrictive levels for longer. They fear that cutting rates too soon could re-ignite demand and undo the progress made on price stability.

The Growth/Employment Risk (The "Doves"):

These Policymakers worried that the lagging effects of high rates, causing a sharp economic slowdown or a spike in unemployment, would push for rate cuts sooner. They argue that policy is already "modestly restrictive" and can be adjusted down "in the near term."

Recent mixed economic reports—such as easing inflation alongside a resilient, though cooling, labor market—are why central bank communication has become so crucial, leading to frequent swings in market expectations.

Market Expectations vs. Central Bank Reality

Market participants, particularly bond traders, constantly try to predict the central bank's next move. They use tools, like the CME Fed Watch Tool, to calculate the probability of a rate hike or cut at upcoming meetings. Remember when rates drop, Bond prices increase, and yield decreases since you pay more for a Bond with a higher coupon

Scenario | Market Expectation Shift | Impact |

Dovish Shift (Rate Cuts Sooner) | Central bank commentary signals slowing economy or lower inflation. | Bond Yields Fall, Bond Prices Rise. Stocks rally (especially growth/tech). |

Hawkish Shift (Rates Stay Higher Longer) | Economic data (e.g., strong jobs, high inflation) is robust. | Bond Yields Rise, Bond Prices Fall. Stocks pull back (higher discount rate). |